How To Win Against CBE Group

Upsolve is a nonprofit that helps you eliminate your debt with our free bankruptcy filing tool. Think TurboTax for bankruptcy. You could be debt-free in as little as 4 months. Featured in Forbes 4x and funded by institutions like Harvard University — so we’ll never ask you for a credit card. See if you qualify →

CBE Group (The CBE Group Inc) is a debt collection agency specializing in consumer debt collection. If CBE Group contacts you, then they have bought a debt of yours from a creditor or lender. Before you pay anything toward the debt, validate it to make sure it is legitimate. Then, figure out how much of the debt you can reasonably pay, and begin debt settlement negotiations. If CBE Group is suing you for unpaid debt, respond to the lawsuit immediately.

Written by the Upsolve Team. Legally reviewed by Jonathan Petts

Updated March 12, 2026

Why Is CBE Group Contacting Me?

CBE Group (also known as The CBE Group Inc) is a debt collection agency that collects consumer debts like medical bills, government entities (local, state, and federal), and utility debt. If you are getting calls and emails from CBE Group, they are attempting to collect on a debt that they think you owe. You need to confirm that the debt is legitimate before you do anything else. This is called validating a debt.

To learn more about CBE Group and what to do if they contact you, read our article How To Deal With CBE Group.

Do I Have To Pay CBE Group?

This depends on whether CBE Group can validate and prove the debt is yours. If CBE Group can validate the debt (and if you agree that the debt is yours), you will most likely have to pay them at least a portion of what you owe. If CBE Group can’t validate the debt, you shouldn’t have to pay them.

Regardless, don’t ignore CBE Group and hope they will disappear. We understand that dealing with debt collectors is stressful, but ignoring them could lead to them filing orders to garnish your bank account or wages.

Even if you do have to pay CBE Group, you might not have to pay them the full amount. You can negotiate a debt settlement, which allows you to pay less than the original debt amount.

How To Negotiate a Debt Settlement With CBE Group in 3 Steps

Debt collection companies are in the business of making money. While that might make them seem intimidating, it can actually work in your favor.

Debt collectors buy debts from creditors/lenders for much less than they’re worth. This means they are typically open to negotiating a debt settlement since they still profit even if you settle to pay a lower amount. Debt collectors will usually settle for 40%–60% of the original amount.

While some debt collectors will initiate a settlement offer, it’s a good idea for you to be the one to start the conversation. This is not as complicated as you might think, and it will feel much less scary once you know the process.

Step 1: Make Sure the Debt Is Valid

If CBE Group hasn’t sent you a debt validation letter, ask them for one as soon as possible. You can create and send a debt verification letter to request information. You need to make sure that:

The debt is yours (sometimes there are mistakes on the collector’s end)

CBE Group legitimately owns the debt

The amount they claim you owe is accurate

The Consumer Financial Protection Bureau (CFPB) outlines a debt collection rule requiring third-party debt collectors to send a debt validation letter before or within five days of contacting you and give you 30 days to dispute the debt. You can use your debt verification letter to dispute the debt.

Step 2: Figure Out What You Can Pay

If you’ve thoroughly reviewed the validation letter and agree that you owe the amount to CBE Group, you must determine how much of the debt you can reasonably pay. Look at your monthly take-home pay, expenses, and existing debt obligations (loans, credit cards, mortgages, etc.).

The CFPB has a helpful budget tool and debt worksheet to help you organize your monthly expenses. If you need extra help, you can get a free consultation with an accredited nonprofit credit counselor.

Once you determine how much of the debt you can pay, you can pick your payment method. Debt collectors prefer one lump-sum payment. If you’re expecting any extra income, like a work bonus or tax return, a lump sum could be an excellent option for you.

If you cannot pay with a lump sum, then suggest a payment plan with monthly payments and a timeline you’re confident in. Some debt collectors will be more open to a payment plan if you set up direct withdrawals from your bank account.

Step 3: Make a Settlement Offer to CBE Group

Once you establish how much you can reasonably pay, it’s time to make CBE Group an offer. You should make your offer in writing and request their reply in writing as well so there’s a record of your conversation.

Upsolve’s Debt Settlement Letter template is a great resource for helping you draft your settlement offer.

Don’t Just Negotiate the Amount… Negotiate Everything!

You don’t have to confine negotiations to the debt amount. You can negotiate other things related to your debt, like how you repay your debt and how the collector reports your account to credit bureaus: “paid in full,” “partial payment,” or “settled.”

Having your debt recorded as “paid in full” is the most beneficial for your credit score, so be sure to include this in your negotiation.

Can You Still Negotiate a Settlement if There’s a Debt Lawsuit Against You?

Usually, yes, you can still negotiate a debt settlement even if a debt collector has filed a lawsuit against you! However, if a debt collector has sued you, continue responding to the lawsuit and following all requirements outlined by the court until your settlement is in writing and submitted, and the court case has been dismissed or closed.

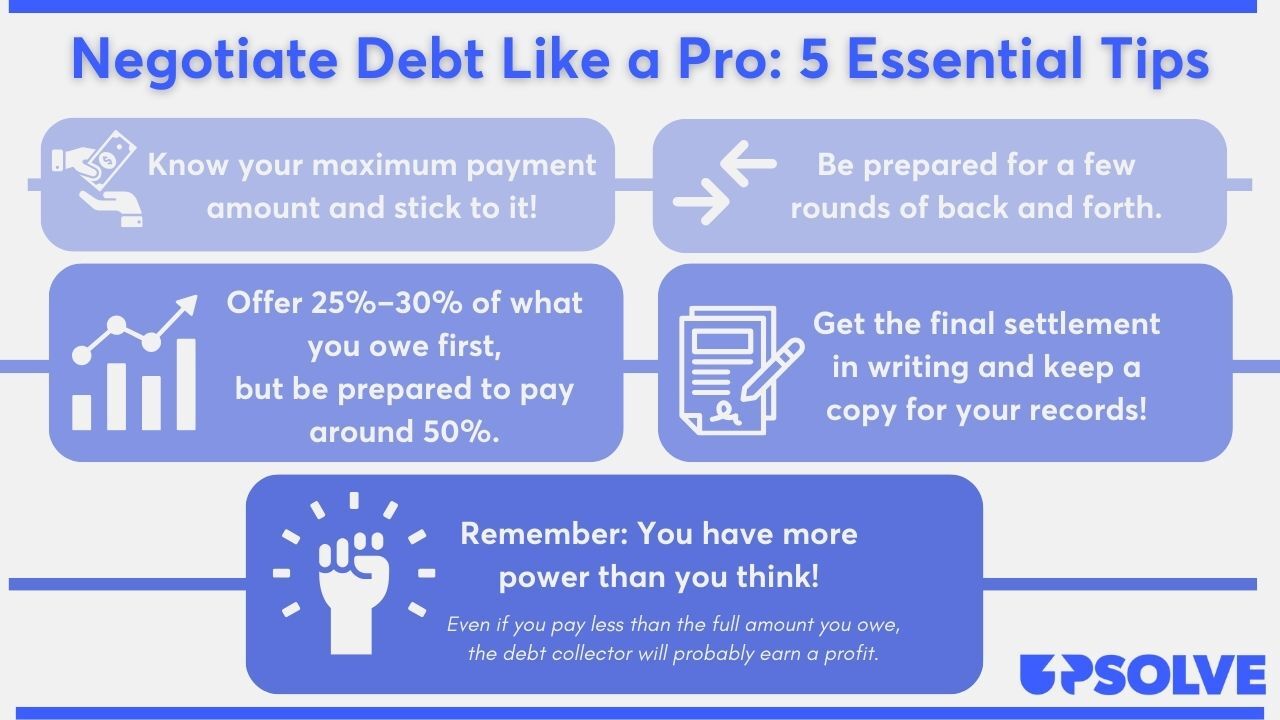

Tips for a Successful Debt Settlement

Negotiating a debt settlement can feel intimidating, but with our essential tips, you’ll be ready to negotiate like a pro.

For even more tips and info, read Upsolve’s article 5 Solid Steps for Negotiating With Debt Collectors.

How To Beat CBE Group in a Debt Lawsuit

If you are sued by CBE Group, you’ll be notified of the lawsuit through a summons and a complaint. These are official documents that alert you to the lawsuit and provide the details of the case.

The most important thing you can do if you are sued is to respond to the lawsuit. If you ignore a debt collection lawsuit, you are putting your finances at risk of a wage or a bank account garnishment.

To respond, you will fill out and file an answer to the lawsuit. Try not to worry; navigating a debt collection lawsuit is easier than you may think.

If you're worried about responding on your own, but you can't afford a lawyer, you can draft an answer letter for free or a small fee using our partner Solo. They've helped hundreds of thousands of people respond to debt lawsuits, and they have a 100% money-back guarantee.

Solo is an affiliate partner, which means Upsolve may earn a small commission if you choose to use their paid service. This helps keep our services free.

Step 1: Read the Summons and Complaint Carefully

A summons is a court document that tells you that a lawsuit has been filed against you. Summons documents vary by court but contain the important details that you’ll need for your answer form, like:

The name and address of the court you report to

Information on all parties involved

The case number assigned to your lawsuit

Details of the legal consequences if you fail to respond to the lawsuit

A complaint is another type of document that will accompany your summons. While the summons alerts you of the lawsuit, the complaint outlines the debt collector's claims against you, usually in numbered paragraphs.

Step 2: Fill Out an Answer Form (and Any Other Required Forms)

Many courts provide blank answer forms for you to respond to the lawsuit.

To find your court’s answer form, try Googling “[court name] + answer form.” Your court should be listed on your summons. Most answer templates also contain instructions for filling out and filing the form, so read these well.

If you don’t understand your court’s forms or processes, reach out to the court clerk, an official who works for the court and can provide administrative assistance. Note: A court clerk cannot give legal advice, only help with forms and court procedures.

The answer form is your opportunity to explain your side of the lawsuit and give affirmative defenses, which are reasons that the debt collector should not win the case. To learn more about debt collection lawsuits and examples of common affirmative defenses, read 3 Steps To Take if a Debt Collector Sues You.

Note: Some courts require you to fill out additional paperwork, like a certificate of service, so make sure you look through your court’s website or talk with the court clerk to learn about your court’s procedures.

Step 3: File the Answer Form With the Court and Serve on the Plaintiff

After completing your answer form, you must submit it to the court detailed in your summons. Most courts offer options for in-person filing, while some provide e-filing systems or accept filings via certified mail. You also probably need to deliver a copy of your answer form to the person suing you (the debt collector) through certified mail.

Filing procedures vary among courts, so look at your court's website or ask the court clerk about your filing options. Your summons should include relevant information, so be sure to review all documents.

Let’s Summarize…

If CBE Group contacts you about a debt, first validate the debt to ensure you actually owe it. If it’s valid, figure out how much you can pay and begin debt settlement negotiations. If CBE Group sues you for unpaid debt, the most important thing you can do is respond to the lawsuit and take action. You may still be able to negotiate a settlement offer, but you must follow all court procedures.