How To Respond to a Virginia Warrant in Debt

Upsolve is a nonprofit that helps you eliminate your debt with our free bankruptcy filing tool. Think TurboTax for bankruptcy. You could be debt-free in as little as 4 months. Featured in Forbes 4x and funded by institutions like Harvard University — so we’ll never ask you for a credit card. See if you qualify →

If you’re sued for a debt that’s $5,000 or less in Virginia, the case will be filed in a general district court. You don’t have to file an answer form to contest the lawsuit, but you must show up to the hearing listed on the Warrant in Debt form. This is the form you’ll get that notifies you that you’ve been sued for a debt. From there, you’ll follow the court’s instructions.

Written by Upsolve Team.

Updated June 5, 2026

How Do Debt Collection Lawsuits in Virginia Work?

Debt collectors are notoriously persistent. Most will try calling you or sending you notices in the mail. If those attempts don’t work, they may decide to bring a debt collection lawsuit against you. If you get sued, you’ll be notified with a document called a Warrant in Debt.

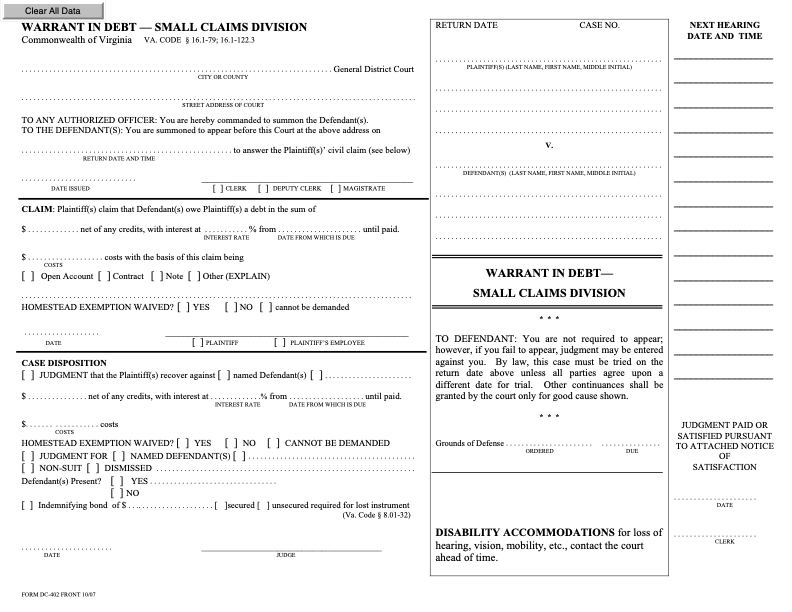

The first page looks like this:

✨If you're worried about responding on your own, but you can't afford a lawyer, you can draft an answer letter for a small fee using Solo. They've helped hundreds of thousands of people respond to debt lawsuits, and they have a 100% money-back guarantee.

Solo is an affiliate partner, which means Upsolve may earn a small commission if you choose to use their paid service. This helps keep our services free.

What Is a Warrant in Debt?

A Warrant in Debt is an official court document that lets you know that a debt collection lawsuit has been filed against you in Virginia.

There’s important information in this document, including:

📍 The court location: This is the name and address of the city or county district court where your case will be heard (found in the top left corner of the form).

🗓️ The return date and time: This is the date and time of your initial court appearance. If you want to challenge the lawsuit, you must show up to this court hearing.

💰 The claim amount: This is the amount the debt collector claims that you owe.

📝 Notice of what happens if you don’t appear: This notifies you that you’re not required to appear for the hearing but that if you don’t, the court can enter a judgment against you. That means the collector automatically wins and can collect the amount they’re asking for.

How Do You Respond to a Virginia Warrant in Debt?

Responding to a Warrant in Debt in Virginia typically involves the following steps:

Attend the scheduled hearing (listed on the Warrant in Debt).

Ask for more detailed information about the debt.

Be prepared to explain your defenses.

Request a trial and await next steps from the court.

Step 1: Show Up to the Scheduled Hearing

The Warrant in Debt will list the date, time, and location of your court hearing. You must attend if you want to respond to the plaintiff’s (the person suing you) claims. If the date or time doesn’t work for you, contact the court clerk as soon as possible to ask about rescheduling.

The first hearing isn’t a full trial. It’s your opportunity to tell the judge you disagree with the claims against you.

💡 It’s a good idea to dress neatly (like you would for a job interview), arrive early, and be respectful — for example, address the judge as “Your Honor.”

Step 2: Ask for More Detailed Information on the Debt

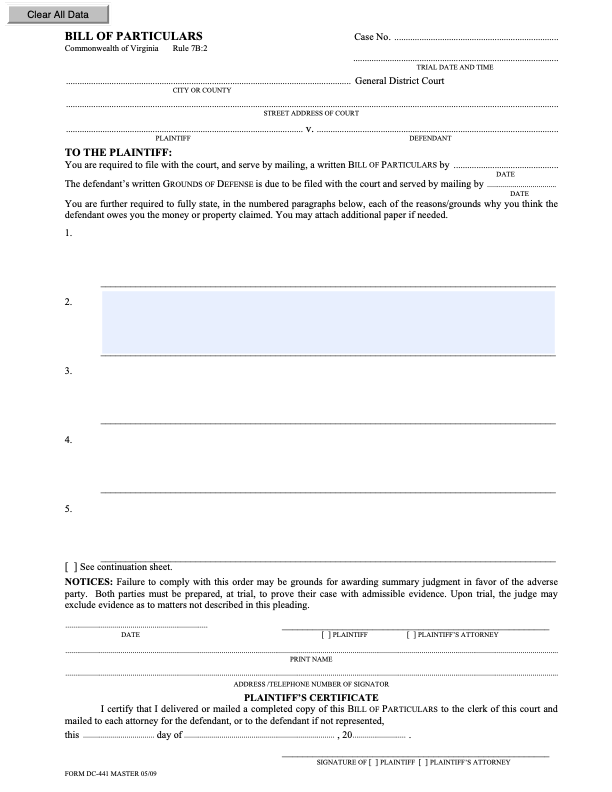

At the hearing, you can ask the judge to require the plaintiff to provide more detailed information about the debt. This is done through a document called a Bill of Particulars, which the plaintiff can be ordered to complete and file with the court.

⚠️ This is an important step. It forces the plaintiff to explain why they believe you owe the debt and to prove that they own the debt and have the legal right to collect it. Be ready to clearly ask the judge for a Bill of Particulars during your hearing.

What Is a Bill of Particulars?

A Bill of Particulars is a formal court document that the plaintiff fills out to explain why they think you owe the debt. It breaks down their claims into numbered sections, listing out the details of what they think you owe and why.

The form looks like this:

🔍 Reading it carefully can help you understand the case against you. It’s also a useful tool to help you figure out how you might want to respond. This can include the defenses you may want to raise.

Step 3: Be Prepared To Explain Your Defenses

Just like you can ask the plaintiff for more information, they can also ask the judge to require you to explain your side in writing.

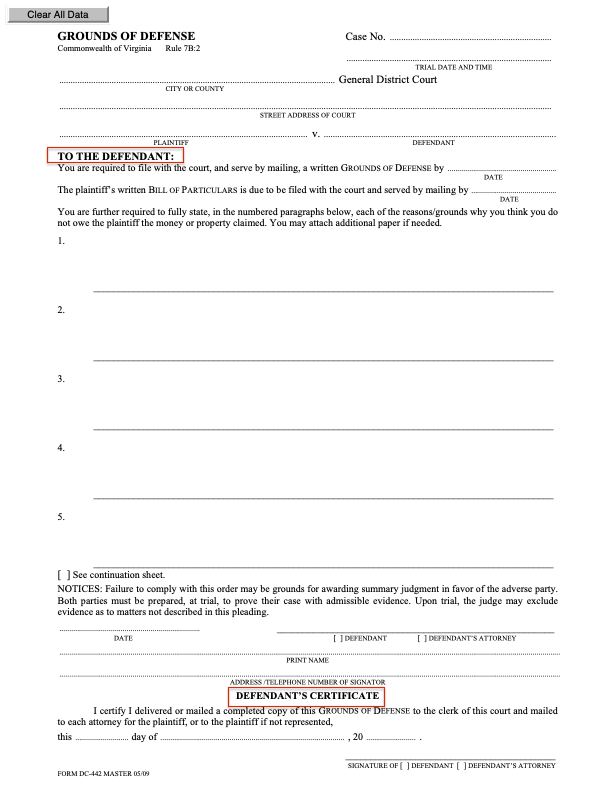

✍️ If that happens, the judge may order you to fill out a form called DC-442 Grounds of Defense. This form gives you space to list your defenses and explain why you don’t think you owe the debt. The court also provides instructions to help you fill it out.

How Do You Fill Out a Grounds of Defense Form?

The Grounds of Defense form is a one-page form that looks like this:

The top portion of the form lists the court’s name and location, along with the names of the parties involved in the case. You are the defendant. The person or company suing you (or their lawyer) is the plaintiff.

The next section, labeled “To the Defendant,'' is where you explain your defenses to the plaintiff’s claims.

💡 If you simply deny what they’ve said, that’s called a defense. But you can also use affirmative defenses. These are reasons that the plaintiff shouldn’t win whether or not their claims are true.

Here are some common affirmative defenses in debt lawsuits:

The debt is too old and the statute of limitations has expired.

You already paid the debt.

The debt was discharged in bankruptcy.

You don’t owe the debt because of identity theft or mistaken identity.

📄 Be sure to include proof to support your defenses and affirmative defenses. This could be in the form of receipts, billing or account statements, letters or emails from the creditor or collector, a credit report, or anything else that helps show your side of the story.

You Must Deliver a Copy of the Grounds of Defense Form to the Plaintiff

The final portion of the form is the “Defendant’s Certificate.” By signing and dating this section, you’re telling the court that you’ve sent a copy of the completed form to the plaintiff or their attorney.

🔎 You can usually find the plaintiff’s name and address on the Warrant in Debt.

You can send the form in the mail or deliver it in person. Just make sure you do this by the deadline listed at the top of the Ground of Defense form. That’s also the deadline to file your copy with the court.

☎️ Most courts accept filings by mail or in person, but it’s a good idea to call the clerk’s office listed on your form to confirm what options are available.

Step 4: Ask for a Trial and Await Next Steps

At your initial court hearing, you can ask for a trial to learn more about the debt the plaintiff says you owe, especially if you’re also requesting a Bill of Particulars.

Going to trial might sound intimidating, but don’t worry. It won’t happen right away. The court will schedule your trial after you’ve received the Bill of Particulars and submitted your Grounds of Defense. By then, you should have a clear picture of why you're being sued and how you plan to respond.

🗣️ At the trial, both you and the plaintiff will have a chance to tell your sides of the story. You’ll speak to the judge, and the judge will make a decision at the end of the trial or sometime after.

📅 Your trial might be scheduled a few months out from your first court appearance. In the meantime, be sure to meet any court deadlines and let the court know if your address changes so you don’t miss important updates.

What Happens if You Don’t Respond to the Lawsuit?

If you don’t respond to the Warrant in Debt, you risk losing the lawsuit by default.

As mentioned above, there’s a notice section in the Warrant in Debt that explains that failing to appear at the scheduled hearing can lead to a judgment. A judgment is a court order. In this case, it’s an order for you to pay what the plaintiff claims you owe.

With a court order in hand, the debt collector may be able to take money directly from your paycheck or bank account through wage garnishment or a bank account levy. Wage garnishment is the most common collection method, but Virginia law limits how much can be taken from each paycheck.

✅ Show up and give yourself a real chance to win the debt collection lawsuit. With the knowledge in this guide, you can respond and defend yourself, without a lawyer’s help.

📝 If the court has already entered a default judgment against you, you may be able to file a motion to have it set aside (canceled). The court provides instructions on how to do this.

Need Legal Help?

If you’re looking for legal help, here are some free or low-cost resources in Virginia:

Virginia Legal Aid offers free legal help for eligible individuals. You can search for help in your area through their Find Legal Help tool.

Virginia Free Legal Answers is an online service from the American Bar Association where you can ask volunteer attorneys questions about your case.

Local law libraries can also be a helpful resource. Librarians can explain Virginia’s legal process and point you toward useful legal materials.