How To Answer a Florida Court Summons for Debt Collection

Upsolve is a nonprofit that helps you eliminate your debt with our free bankruptcy filing tool. Think TurboTax for bankruptcy. You could be debt-free in as little as 4 months. Featured in Forbes 4x and funded by institutions like Harvard University — so we’ll never ask you for a credit card. See if you qualify →

If you�’re sued for a debt that’s less than $8,000 in Florida, your case will be a small claims case heard in a county court. You’ll receive notice of the lawsuit with a summons and complaint. You need to respond to the lawsuit by filing an answer form with the court and sending a copy to the person suing you. If you don’t, you risk having the judge rule against you without getting to tell your side of the story. Losing the case can result in wage garnishment or a bank account levy.

Written by Upsolve Team.

Updated August 25, 2025

How Do Debt Collection Lawsuits in Florida Work?

If you’re being pursued for an outstanding debt, the debt collector or creditor may eventually decide to sue you. Debt collection lawsuits are civil actions (as opposed to criminal). In Florida, if you’re being sued for $8,000 or less, the case will be considered a small claims case, and it will be heard in a county court.

Anything over $8,000 but less than $50,000 will be heard in county civil court, but this is rare for debt lawsuits.

You’ll know you’ve been sued because you’ll receive official documents notifying you of the claim against you. These documents are known as a summons and complaint. In Florida small claims courts, the complaint is often referred to as the “statement of claim.”

To get a sense of the overall process, you can visit the Florida Courts Small Claims page. The Process: What Happens in Court, prepared by the Florida Courts Help, is also helpful. It’s written for family court matters, but much of the information applies to any civil case, including small claims debt collection cases.

If you've been sued for a debt but you can't afford a lawyer, you can draft an answer letter for a small fee using SoloSuit. They've helped over 340,000 people respond to debt lawsuits, and they have a 100% money-back guarantee.

SoloSuit is an affiliate partner, which means Upsolve may earn a small commission if you choose to use their paid service. This helps keep our services free.

What Is a Summons and Complaint?

A summons is a legal document that informs you of a lawsuit against you.

A complaint is a legal document that outlines the plaintiff’s (the person suing you) claim(s) against you, often in numbered paragraphs.

The summons typically includes the contact information of the person or firm bringing the lawsuit. For debt collection cases, this will often be a law firm representing the creditor or debt collector. It should also list the date by which you must submit your answer to the court. The answer is your way of letting the court know that you are responding to the lawsuit. The summons will also probably include basic information on what next steps you need to take.

The complaint or statement of claim will also list the amount the debt collector believes you owe and what remedy they seek. This is usually in the form of a money judgment, which is a court order requiring you to pay the amount in the complaint plus other costs like legal fees or court costs.

What Happens if You Don’t Respond to the Lawsuit?

You may face serious consequences if you don’t respond to the lawsuit. The court is likely to issue a default judgment in the plaintiff’s favor. The plaintiff is the person who’s suing you. Having a judgment will allow them to access collection measures like a wage garnishment or a bank account levy.

With wage garnishment, money is taken directly from your paycheck. (Though there are some exceptions if you the head of household.) With a bank levy, money is taken directly from your bank account. Debt collectors can only do this if they have a court order. Responding to the lawsuit is the best way to potentially stop it.

Also, consider this: Most debt collectors are counting on you simply not responding to the debt collection lawsuit. They want an easy win. Simply filing an answer may be enough to cause the debt collector to drop the lawsuit. If they don’t, it’s possible for you to win the debt collection lawsuit, even if you don’t hire an attorney.

✨ If you’re overwhelmed by debt or already facing a default judgment, filing bankruptcy may be one way to stop collection actions like wage garnishment or bank levies. If your case is simple, Upsolve’s free filing tool may be able to help.

How To Answer a Florida Court Summons for Debt Collection

To respond to the debt collector’s lawsuit in Florida, you simply need to file an answer with the county court within 20 days of being served with the summons and deliver a copy of your answer form to the person suing you.

There is more information on how to do this below, but if you find you need additional help, you can speak with the clerk of court, find a self-help center, or visit a law library to get assistance.

File an Answer to the Summons Within 20 Days

After being served with the summons and complaint, you’ll have 20 days, including weekends and holidays, to file your answer with the court (and send a copy to the person suing you).

The answer form is a legal document. In it you will indicate whether you admit, deny, or don’t have knowledge of each claim lodged against you. Then you can list and explain any defenses you have. Be sure to number each of your explanations and refer to the paragraph numbers used in the complaint. You can also attach copies of any documents that support your defenses.

Community Legal Services of Florida has good information about possible defenses you could raise in your case. If the debt collector has broken any state or federal laws, you may be able to raise this as a defense. To learn more, read our guide to Florida’s debt collection laws.

Use DIY Florida To Generate Your Answer Form

Most people have never drafted a court document before, so it can feel intimidating. The Florida courts have made it easier by offering DIY Florida.

This is an online service that asks you simple questions about your case and then creates the legal documents you need — in this case, the answer form — for free. Further, it allows you to file the form online, so you don’t have to go to the courthouse in person.

Create Your Own Answer

If you don’t want to use DIY Florida, you can view this sample answer form from Jax Legal Aid to get a sense of what the form looks like and what information it should include. In addition to the items listed above, you’ll also want to list the names of both parties in the case, the court name and division, and the case number.

However you create your answer form, make at least two copies of it when it’s complete. One for the court clerk and one for the plaintiff. It’s also a good idea to make a copy for your own records.

If you don’t file your answer online with the court, you’ll need to deliver it in person to the clerk of court at the county courthouse listed on the summons.

Serve a Copy of the Answer on the Plaintiff

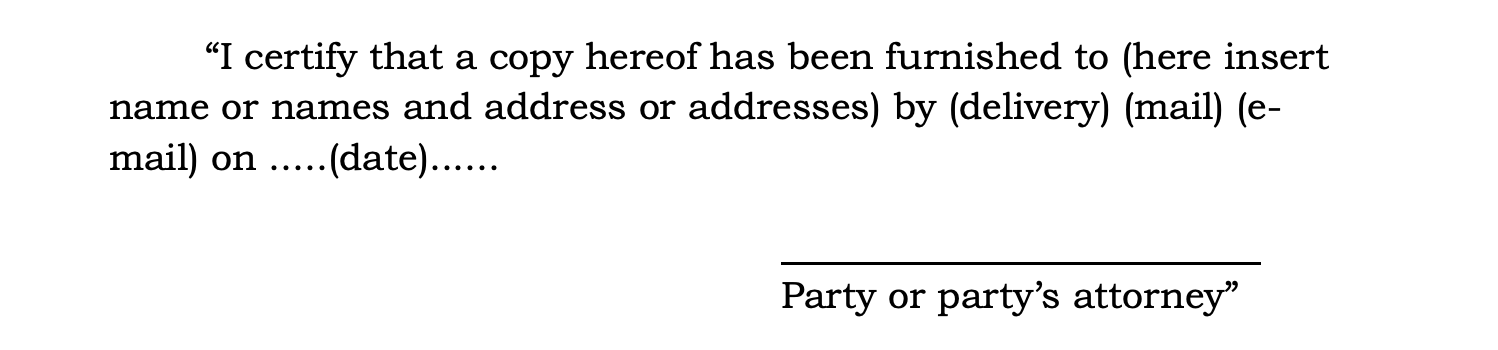

In legal terms, service means proper delivery. When you serve papers on another party, you have formally delivered them however is required by the court. This could be by mail, personal delivery, or email. You may also be required to submit a certificate of service to the court. The clerk will tell you exactly what’s needed.

Here’s an example of a service certificate from the Florida Small Claims Rules:

You must serve your answer on the plaintiff in the debt collection case. You can usually email the papers to the attorney representing the plaintiff.

Ask your county court clerk to be sure you serve your papers correctly. Use this court directory to search for your clerk by county. Clerks can’t give you legal advice about your case, but they are excellent resources for information on court processes and rules.

What Happens Next?

After you file your answer and serve it on the plaintiff, you’ll likely get court documents notifying you of a pre-trial conference at the county court (or remotely). Follow the instructions on the documents you get and be sure to show up for any scheduled appearances. If you’re unable to attend, call the county clerk and ask how to file for a continuance or reschedule the hearing date.

The creditor or debt collector may also reach out to you to try to settle the debt. If you decide to participate in a debt settlement, it’s important that you continue to keep up with the court case as well! Show up for any required appearances and follow all other instructions the court sends you. This protects you in case the debt collector is acting in bad faith or you aren’t able to reach a settlement agreement.

SoloSuit can also help you with debt settlement if you use their service to respond to your debt lawsuit.

How To Prepare for Court Appearances

Going to court may feel intimidating. The good news is that small claims cases tend to be less formal than other types of lawsuits. Though there will probably be fewer court rules and procedural requirements, it’s still important to get familiar with what’s expected of you.

Generally speaking, it’s a good idea to arrive early for your hearing, speak respectfully to the judge, dress professionally, and come prepared with any documentation that supports your case.

You can watch this video from Florida Courts Help on Preparing for Court: Courtroom Expectations to learn more.

What Do You Do if the Court Already Issued a Default Judgment Against You?

If a Florida county court judge has already issued a default judgment against you, you may be able to file a motion for relief from judgment. Most motions must be filed within one year of the judgment being entered. A motion is a formal request asking the court to take a specific action. In the end, it boils down to more paperwork.

There are only a few reasons the court views as valid for granting a relief from judgment, including:

There was a clerical mistake.

There is newly discovered evidence.

Fraud was committed.

You may wish to get legal advice before filing a motion for relief. Many attorneys offer free consultations. The court provides a comprehensive list of legal aid resources throughout the state.