How To Win Against Harris & Harris

Upsolve is a nonprofit that helps erase your debt with our free bankruptcy filing tool. You could be debt-free in just 4 months. See if you qualify→

Upsolve is a nonprofit that erases your debt with our free bankruptcy filing tool. See if you qualify.

If Harris & Harris contacts you, respond and take action, as they are a recognized debt collection agency. Before you pay anything, validate the debt to confirm it is accurate and yours. If the debt is legitimate, you need to figure out how much of the debt you can pay and begin debt settlement negotiations. If Harris & Harris is suing you for unpaid debt, you can respond by using an answer form — even if you’re in the middle of negotiating or settling — and following your court’s procedures.

Written by the Upsolve Team. Legally reviewed by Jonathan Petts

Updated March 12, 2026

Why Is Harris & Harris Contacting Me?

Harris & Harris is a debt collection agency that collects consumer debts, specifically for healthcare and utility companies and government entities.

If Harris & Harris contacts you, it’s probably because the original creditor of your debt has sold your debt to the debt collection agency. Harris & Harris will then create an account in your name and take over the process of collecting payment from you via written notices and phone calls. To learn more about Harris & Harris and what to do if they contact you, read our article How To Deal With Harris & Harris.

Do I Have To Pay Harris & Harris?

The short answer is maybe. Whether you have to pay Harris & Harris depends on whether they can validate the debt and prove it is yours.

If they can validate the debt — and if you agree that the debt is yours — you will probably have to pay them. If Harris & Harris can’t validate the debt, you shouldn’t have to pay them, and they should stop contacting you.

If the debt is valid, your main options for moving forward are to dispute the debt (if the information is incorrect or you disagree with the debt amount), pay the debt in full, or negotiate a settlement so you only pay a portion of the debt.

What happens if Harris & Harris validates the debt and you don’t pay? Unfortunately, if you ignore a legitimate debt and Harris & Harris sues you and wins, you could face serious consequences. They can win court orders like bank account garnishments or wage garnishments and take your income.

Even if you have to pay Harris & Harris, you may not have to pay them the total debt amount. You can work with them to negotiate a debt settlement where you pay less than the original amount.

How To Negotiate a Debt Settlement With Harris & Harris in 3 Steps

Third-party debt collection companies like Harris & Harris are businesses. Their main objective is to make money, which actually gives you an edge in negotiations. How?

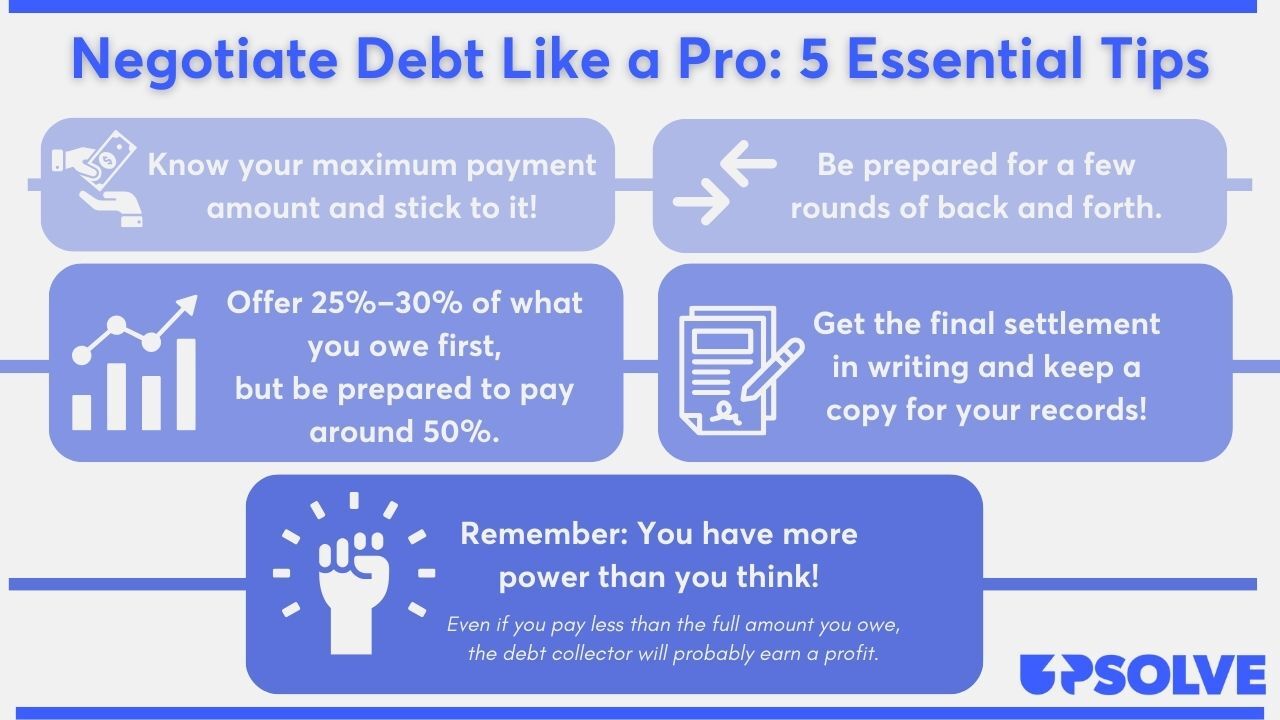

Debt collectors typically buy debts from creditors or lenders for less than the debt is worth. This means they are usually open to negotiating your debt because they still make money even if you settle the account for less. A lot of debt collectors will settle for 40%–60% of the original debt.

The debt collector may be the one to reach out with a settlement offer, but if you’re the one to initiate the conversation, you might get the upper hand. This process probably sounds intimidating, but knowing the ins and outs can give you the confidence you need to negotiate successfully.

Step 1: Make Sure the Debt Is Valid

If Harris & Harris hasn’t sent you a debt validation letter, ask them for one. Once you get your debt validation letter, read it thoroughly and verify all information. You want to make sure the debt is yours, that Harris & Harris owns it, and that the amount is correct.

The Consumer Financial Protection Bureau’s (CFPB) debt collection rule requires third-party debt collectors to send debt validation letters. Collectors also must give you 30 days to dispute the debt. The letter should explain the dispute process.

If Harris & Harris hasn’t sent you a validation notice or if their notice didn’t provide all the information you need to verify the debt, you can send them a debt verification letter.

For more information on debt validation letters versus debt verification letters, check out our image below:

Step 2: Figure Out What You Can Pay

Next, you need to figure out how much of your debt you can reasonably pay Harris & Harris. Look at your monthly take-home pay and expenses and your existing debt obligations, such as loans, credit cards, or a mortgage.

The CFPB has a budget worksheet to help you with this process. They also have a debt worksheet that helps you visualize your bills and analyze your expenses. If you need extra help, you can get a free consultation with an accredited nonprofit credit counselor.

Once you determine how much you can pay, choose how to pay Harris & Harris. Debt collectors typically prefer a lump-sum payment. If you have an extra boost in income — like a work bonus or a recent tax return — this could be a good route for you.

If a lump-sum payment isn’t realistic, you can suggest a payment plan with reasonable monthly payments and a timeline you’re confident in. Debt collectors may be more open to this option if you set up a direct withdrawal from your bank account.

Step 3: Make a Settlement Offer to Harris & Harris

Now that you know how much of the debt you can pay, make Harris & Harris an offer. It’s smart to make your offer in writing and request their reply in writing. This way, you have documentation of your exchange.

You can use Upsolve’s Debt Settlement Letter template to craft your offer letter.

Don’t Just Negotiate the Amount… Negotiate Everything!

Know that you have the option to negotiate beyond the settlement amount! You can also negotiate how you repay your debt and how the collector reports your account to credit bureaus.

Collectors can report your account as paid in full, partial payment, or settled. Having your debt marked “paid in full” is the most beneficial for your credit score, so this is important to negotiate.

Can You Still Negotiate a Settlement if There’s a Debt Lawsuit Against You?

In a lot of cases, yes, you can still negotiate a debt settlement even if Harris & Harris is suing you.

The most important thing you can do if you’re involved in a lawsuit is to respond. If you’re in the middle of debt settlement negotiations, you still need to follow all requirements, like court appearances, until your settlement is in writing and submitted to the court.

Tips for a Successful Debt Settlement

If you’ve never been in negotiations before, it can feel intimidating. Check out our top tips on how to negotiate like a total pro:

For more tips and info on the art of negotiations, read Upsolve’s article 5 Solid Steps for Negotiating With Debt Collectors.

How To Beat Harris & Harris in a Debt Lawsuit

If Harris & Harris sues you, you’ll be notified of the lawsuit through two official documents: a summons and a complaint.

You can respond to the lawsuit by filing an answer form and following any other instructions listed on your summons. If you ignore a debt collection lawsuit, the judge will most likely rule against you. Then, Harris & Harris can get a court order to garnish your wages or bank account. Don’t panic, though — responding to a lawsuit is easier than you’d think.

If you're worried about responding on your own, but you can't afford a lawyer, you can draft an answer letter for free or a small fee using our partner Solo. They've helped hundreds of thousands of people respond to debt lawsuits, and they have a 100% money-back guarantee.

Solo is an affiliate partner, which means Upsolve may earn a small commission if you choose to use their paid service. This helps keep our services free.

Step 1: Read the Summons and Complaint Carefully

A summons is a court document that notifies you of a lawsuit. The summons has important details that you’ll need for your answer form, including:

The name and address of the court you report to

Information on all parties involved

The case number assigned to your lawsuit

Details of the legal consequences if you fail to respond to the lawsuit

Summons documents vary from court to court, but they usually contain all the key information you need to know about your lawsuit.

A complaint will usually come with your summons form. While the summons alerts you of the lawsuit, the complaint outlines all of the debt collector’s claims against you.

Step 2: Fill Out an Answer Form (and Any Other Required Forms)

You can respond to a lawsuit by filling out and filing an answer form — blank answer forms can often be found on your court’s website. They should also have instructions on how to fill out and file the form. To find your court’s answer form, try Googling “[court name] + answer form.”

If you don’t understand the questions on the answer form, reach out to the court clerk. The clerk is a court official who provides administrative help with paperwork and helps people navigate court rules. They can’t give you legal advice, but if you need legal help, they may be able to point you to free or low-cost legal resources.

The answer form is where you explain your defenses or affirmative defenses. It gives you the chance to confirm or deny each claim made against you and add any additional information the debt collector may have left out. To learn more, read our article about debt collection lawsuits common affirmative defenses.

Step 3: File the Answer Form With the Court and Serve on the Plaintiff

After filling out your answer form, file it with the court and deliver a copy to Harris & Harris. The instructions for this should be listed on your summons or answer form. Most courts allow you to file your form in person or mail the form in. If you mail your form, it’s best to send it using certified mail. Some courts allow you to email or e-file your form.

Again, each court has its own filing procedures and rules, so check your summons, answer form, or the court’s website for instructions. You can also ask the court clerk about your filing options.

Let’s Summarize…

Harris & Harris is a legitimate debt collection agency that collects consumer debts for healthcare and utility companies and government entities. If Harris & Harris is contacting you, they probably bought a debt that they believe you owe. You need to validate that debt, figure out how much of the debt you can pay, and begin debt settlement negotiations. If Harris & Harris is suing you for unpaid debt, the most important thing you can do is respond to the lawsuit by filing an answer form.