How To Win Against FBCS

Upsolve is a nonprofit that helps you eliminate your debt with our free bankruptcy filing tool. Think TurboTax for bankruptcy. You could be debt-free in as little as 4 months. Featured in Forbes 4x and funded by institutions like Harvard University — so we’ll never ask you for a credit card. See if you qualify

FBCS is a third-party debt collector, so if they contact you, they’re probably trying to collect on a debt account. Before you pay anything, have FBCS validate the debt and confirm its details. Then you can decide what to do next. If you disagree with any aspect of the debt, you can file a dispute. If you agree you owe the debt and want to pay it, you can pay it in full or try to settle the debt for less than the full amount. If FBCS sues you, you’ll need to respond to the lawsuit.

Written by the Upsolve Team. Legally reviewed by Jonathan Petts

Updated May 8, 2025

Why Is FBCS Contacting Me?

FBCS is a third-party debt collection company that collects consumer and commercial debts. If FBCS calls you or sends you a letter, it’s probably trying to collect a past-due bill that it purchased from a credit card company, bank, utility company, or healthcare provider. Alternatively, FBCS might be collecting a debt on behalf of a creditor. Either way, ask FBCS to send you a debt validation notice so you can make sure the debt is legit before you decide what to do next.

To learn more about FBCS, you can read Upsolve’s article, How to Deal with FBCS.

Do I Have To Pay FBCS?

If FBCS can validate the debt and you agree the debt is yours and the amount is correct, it’s usually best to figure out how to pay it. If you don’t, your credit score may drop, and FBCS may eventually sue you. If they win the lawsuit, they can get a court order to garnish your paycheck or freeze your bank account.

If you want to pay the debt off, but you don’t have the funds to pay it in full, you may be able to negotiate your debt amount down.

How To Negotiate a Debt Settlement With FBCS in 3 Steps

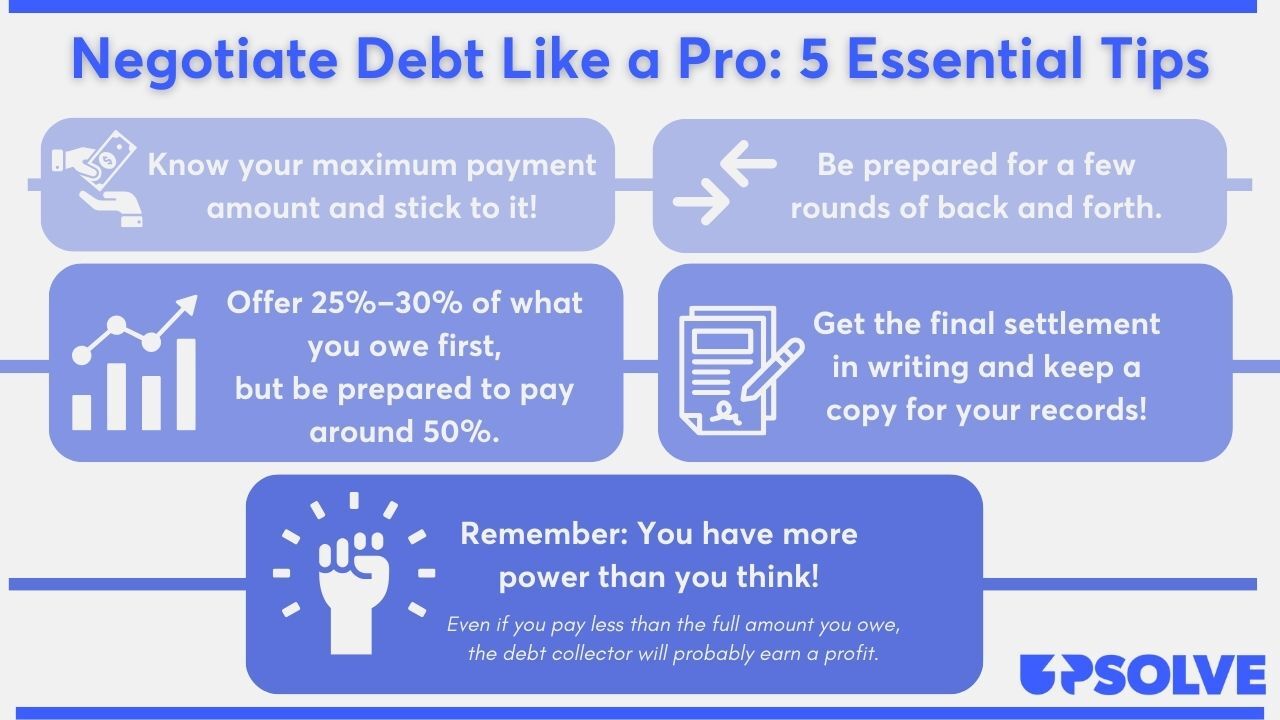

Debt collectors like FBCS usually make money by buying debts from creditors who give up on collecting the debt. They usually buy debt accounts in large batches for a fraction of what you owe. This is why they’re often willing to negotiate. They probably didn’t pay the full amount of your debt, so if they can get you to pay even 40%–60%, they can still earn a profit.

FBCS may reach out with a settlement offer, but you don’t have to wait. You can take the first step. And it’s not as difficult as you might think once you learn how it works.

Step 1: Make Sure the Debt Is Valid

Before you start negotiating, confirm the details of the debt! You don’t want to pay what isn’t yours or that you’ve already paid.

Some people assume that if a debt collector has contacted them, they owe what the collector says they owe. But debt collectors like FBCS get information wrong more often than you might think. This is why the Consumer Financial Protection Bureau (CFPB) has a debt collection rule requiring third-party debt collectors to send validation notices.

FBCS should send you a validation letter before they contact you or within the first five days of contacting you. The validation notice must inform you of your right to dispute the debt within 30 days and give you information about how to do so. That’s all according to the CFPB’s collection rule. Use this letter to verify that the debt account is yours, FBCS has permission to collect the debt, and the debt amount is accurate.

If you want more details than FBCS included in the validation notice, you can send a debt verification letter with further questions.

Step 2: Figure Out What You Can Pay

You may not be able to pay the debt in full, but if you can pay something, you have enough to start a negotiation. First, you have to figure out how much you could pay.

If you’re starting from scratch, you can use the CFPB’s budget tool and debt worksheet to help you understand your income and expenses and what, if anything, is left over each month. If this feels super stressful, take a breath and consider scheduling a free consultation with an accredited nonprofit credit counselor. They can support you as you figure out your budget, and they can go over your other debt-relief options.

Also, keep in mind any windfalls — no matter their size — that might come your way. The most common are tax refunds or work bonuses. You can create your own windfall if you’re able to sell some items for extra cash or work a side hustle for a little while. If you can round up a decent amount, you can offer a lump-sum payment. Which brings us to the next point…

Figure Out How You Can Pay

You usually have two repayment options: a monthly payment plan or a lump-sum payment. If you can afford to make a lump-sum payment, you may be able to negotiate a lower settlement amount. That’s because the debt collector can close the account for good once they get paid. If you negotiate a payment plan but miss one or more payments, the debt collector has to do more work. So you may be able to negotiate for a monthly payment plan, but you might end up paying more in the long run.

Companies like FBCS are usually more likely to accept settlement offers with lump-sum payments, but it’s not easy for most people to come up with enough cash to do this. So if a monthly payment plan is your only option, figure out how much you can afford to pay each month and how long it will take to pay off the debt.

A large monthly payment with a short repayment period will be the most attractive to companies like FBCS. You can also sweeten the deal by offering to have the payment withdrawn directly from your bank account. Only offer this if you’re confident the money will be there when the payment date rolls around. Avoid getting in deeper financial trouble with overdraft fees.

No matter what amount you end up offering FBCS, remember that it should be something you can reasonably afford. And give yourself some wiggle room for the unexpected, such as a temporary dip in income or an unforeseen bill.

Step 3: Make a Settlement Offer to FBCS

Once you know how much you can afford to pay FBCS, it’s time to make an offer. The golden rule of negotiation is to start with a lower number than what you’re ultimately willing to pay. If FBCS accepts your initial offer, great! But don’t be surprised or discouraged if there’s some back and forth. This is common.

Also, when you make your offer, do so in writing. You can use Upsolve’s debt settlement letter template to get started. Ask FBCS to respond in writing, too. This ensures you have a record of your exchange and whatever you agree on. If you make any agreements over the phone, write down what was said and ask the FBCS representative to send you a written confirmation.

Don’t Just Negotiate the Amount… Negotiate Everything!

The debt settlement amount matters a lot, but there are other things you can negotiate, too. As already mentioned, you can negotiate whether you pay in a lump sum or with monthly payments. You can also negotiate how long you get to repay the debt.

But one often overlooked bargaining chip is how your account shows up on your credit report, which can impact your credit score. When debt accounts are settled, debt collectors often report them as “partial payment” or “settled.” But you can ask them to report the account as “paid in full,” which will be better for your credit score than “partial payment” or “settled.” This can be really helpful if you’re working on repairing your credit score.

Tips for a Successful Debt Settlement

Negotiating with a debt collector can seem intimidating. Here are some tips to improve the chances of a successful debt settlement.

To learn more tips and strategies, read Upsolve’s article 5 Solid Steps for Negotiating With Debt Collectors.

How To Beat FBCS in a Debt Lawsuit

If FBCS can’t collect a debt from you despite their best efforts, they might sue you. If they do, you’ll receive documents from the court, typically in the form of a summons and a complaint. If you don’t respond to the complaint, FBCS will probably win the case by default. If they win, they can ask for a court order to take money from your paycheck.

If you're worried about responding on your own, but you can't afford a lawyer, you can draft a answer letter for free or a small fee using our partner SoloSuit. They've helped 234,000 people respond to debt lawsuits, and they have a 100% money-back guarantee.

Responding to a lawsuit might seem hard, but it’s probably not as difficult as you fear. Here are the three steps you can follow to respond to a debt lawsuit on your own.

Step 1: Read the Summons and Complaint Carefully

A summons is an official court document that tells you you’re being sued. It usually also tells you:

The court name and address

The names and addresses of the parties in the lawsuit (you would be the defendant and the FBCS would be the plaintiff)

The case number and nature of the lawsuit

A list of legal consequences for failing to respond to the lawsuit

Deadline to respond to the lawsuit (given as the number of days you have to respond or the date your response is due)

The complaint is a legal document that usually accompanies a summons. It lists the debt collector’s claims against you, usually in numbered paragraphs. When you fill out your answer form, you can admit, deny, or say you don’t have enough information to admit or deny each of the debt collector’s claims. Read each one carefully.

Step 2: Fill Out an Answer Form (and Any Other Required Forms)

An answer is a form you fill out to formally respond to the lawsuit. Some courts have blank forms you can use as a template for your answer. To see if your court has an answer form you can use to get started, Google the name of your court plus “court forms” or “answer form.” If you can’t find the forms online, you can call the court and ask if they have a hard copy you can pick up.

Some, but not all, answer forms also have a page of instructions. Read these carefully. If you need help finding a form, understanding something on the form, or understanding the court’s rules, you can ask the court clerk. These court officials can’t give legal advice, but they are pros at helping non-lawyers decode legal rules.

The answer form may ask for your defenses. You can learn more about common defenses for debt collection lawsuits in Upsolve’s article 3 Steps To Take if a Debt Collector Sues You.

Some courts will require additional forms, like a certificate of service. Since every court is different, check your court’s website or ask the court clerk about additional required forms.

Step 3: File the Answer Form With the Court and Serve on the Plaintiff

After you complete your answer and any other necessary forms, file them with the court and deliver a copy to the plaintiff (the person suing as listed in the summons).

The exact process for how to file forms depends on your court, but you can typically file forms in person at the courthouse or via mail. Less commonly, you may be able to email or e-file the form with the court. The summons may tell you your options. If it doesn’t, research on the court’s website or ask the clerk.

Research or ask the court about the “process of service” rules. This will guide you in properly delivering a copy of the form to the plaintiff, which is typically required. Often, you can deliver the form in person (or ask someone else to do it) or send it via mail. When you mail court forms, it’s advisable to do so using certified mail so you have proof of the mailing.

Can You Still Negotiate a Settlement if There’s a Debt Lawsuit Against You?

Yes, you can usually still settle a debt after you’ve been sued. However, if you enter into settlement negotiations with FBCS, you should also continue to respond to the lawsuit unless and until the case is officially closed or dismissed.

Let’s Summarize…

If FBCS contacts you, they’re probably trying to collect a debt from you. Ask FBCS to validate the debt before you do anything else. If they validate it, but you disagree with the debt account or amount, dispute it. If you agree with the debt and it’s valid, it’s time to figure out how to pay it.

FBCS may be open to negotiating a debt settlement, which allows you to pay less than the full amount of the debt. If you can’t come to a resolution, FBCS may sue you, but you can still fight back.