How To Win Against RMP Services

Upsolve is a nonprofit that helps you eliminate your debt with our free bankruptcy filing tool. Think TurboTax for bankruptcy. You could be debt-free in as little as 4 months. Featured in Forbes 4x and funded by institutions like Harvard University — so we’ll never ask you for a credit card. See if you qualify →

RMP Services is a debt collector that works exclusively for healthcare companies. If they contact you, they likely bought a past-due account from a healthcare provider and are looking to collect on it. Before you pay anything, validate the debt to ensure it’s legitimate. If the debt is genuine, you probably have to pay or risk serious consequences. If you can’t afford the full amount, make a debt settlement offer to repay a fraction of the original debt amount and close the account for good. If RMP Services sues you, respond ASAP by filing an answer form with your court.

Written by Attorney Tina Tran. Legally reviewed by Jonathan Petts

Updated March 12, 2026

Why Is RMP Services Contacting Me?

Receivables Management Partners LLC, known as RMP Services, is a third-party debt collection agency that collects past-due payments for healthcare companies. If they contact you, they likely bought a debt of yours from your healthcare provider and are looking to resolve the debt.

You can learn more about RMP Services in Upsolve’s article How To Deal With RMP Services.

Do I Have To Pay RMP Services?

The short answer is: maybe. Whether or not you have to pay RMP Services depends on if they can validate your debt. You shouldn't have to pay if they can’t validate your debt. If this happens, it’s best to dispute the debt rather than ignore it.

If RMP can validate the debt, you likely have to pay, or you risk opening yourself up to some serious legal consequences. They could sue you to get a court order for wage garnishment or a bank levy. Either allows them to take your hard-earned money.

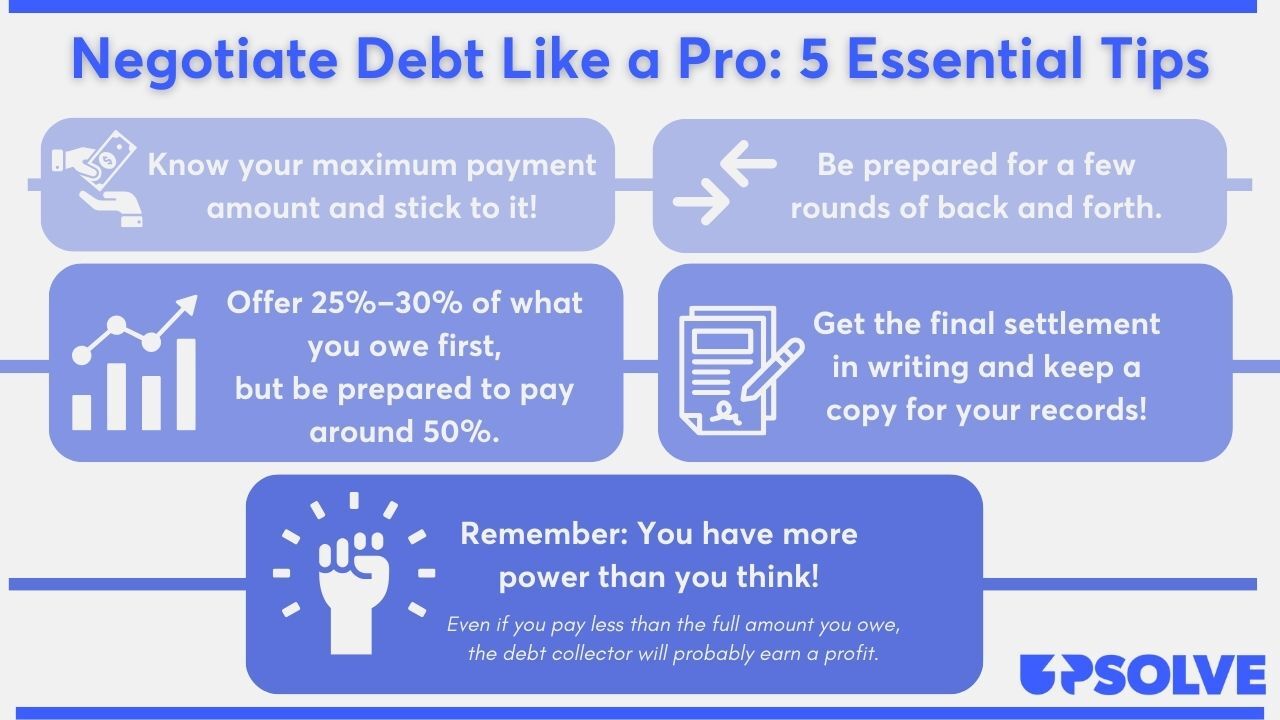

If you haven’t paid this debt because you can’t afford to repay the full amount, try negotiating a settlement with RMP Services. This allows you to clear your debt without paying the entire amount. Here’s how to settle a debt in just three steps.

How To Negotiate a Debt Settlement With RMP Services in 3 Steps

You might not feel like you have any sway when negotiating with a collection agency, but you have more power than you think.

Debt collectors are usually open to negotiating because they buy debt(s) from creditors for pennies on the dollar. This means they make a profit even if you settle with them for less than the original debt total. Start negotiations low — as low as 25% of the original amount — and be ready for some back and forth. Most debt collectors will settle for 40%–60% of your original debt total.

Though it might feel intimidating, it’s a good idea to initiate the negotiation process. You can gain some confidence by reading about the process below.

Step 1: Make Sure the Debt Is Valid

Before anything else, you need to make sure the debt is valid and belongs to you. RMP Services should send you a validation letter. This is required of all third-party debt collectors under a debt collection rule made by the Consumer Financial Protection Bureau (CFPB). The same rule requires them to give you 30 days to dispute the debt. If they haven’t sent a debt validation letter, ask for one right away.

Use the information in the debt validation notice to confirm with your own records that:

The debt account really belongs to you

RMP Services actually owns the debt or has the legal authority to collect it

The debt amount is correct

If you need more information about the debt or if you choose to dispute the debt, a debt verification letter can come in handy.

Here is a simple breakdown of the main differences between a debt validation letter and a debt verification letter:

Step 2: Figure Out What You Can Pay

Before you make a settlement offer, you need to decide how much of the debt you can pay. Take a look at your monthly income and expenses and see how much money you have left over. The CFPB has a helpful budgeting worksheet and debt worksheet if you need some guidance on your budgeting process.

If you’re looking for further help, contact an accredited nonprofit credit counselor for a free consultation. Taking a close look at your finances can feel intimidating, so don’t hesitate to reach out to a professional for help.

Once you figure out how much of the debt you can comfortably pay, decide what method of repayment works best for you.

Lump-Sum Payment vs. Payment Plan: Which Is Better?

Let your financial situation guide you to the right repayment path. If you have any savings you can bear to part with or if you’re expecting a small windfall — like a tax return or employment bonus — a lump sum could be a good route for you. Offering a lump sum is usually the best way to negotiate the lowest repayment amount.

If a lump-sum payment isn’t viable for you, that’s okay. A repayment plan may be a better idea. Figure out what monthly payment amount will work for your budget, pick a timeline you feel confident in, and consider setting up an automatic monthly withdrawal from your bank account. This could help RMP Services feel more open to accepting your payment plan settlement offer.

Step 3: Make a Settlement Offer to RMP Services

Now it’s time to make RMP Service a debt settlement offer. It’s best to make this offer over the phone, but if you choose to make your offer in writing, you can use Upsolve’s Debt Settlement Letter template to craft your letter.

How Do Medical Bills Affect Your Credit Score?

When you receive notice that any account of yours has been sent to collections, it’s a good idea to check your credit report. You can get a free credit report every week from AnnualCreditReport.com.

Be aware that medical debt is treated differently than other kinds of debt on your credit report. According to the CFPB, the following medical debts should not appear on your credit report or affect your credit score:

Medical collections accounts under $500

Paid medical collections accounts

Medical collections accounts that are less than a year old

If any of these appear on your credit report, you have the right to dispute them to have them removed. This is a good way to help boost your credit score.

Can You Still Negotiate a Settlement if There’s a Debt Lawsuit Against You?

Usually, yes, you can still negotiate a debt settlement even if a collector files a lawsuit against you. That said, you still need to participate in the lawsuit and show up to court appearances until the lawsuit is dismissed or closed.

Tips for a Successful Debt Settlement

Negotiating with a debt collector may seem intimidating, but once you arm yourself with the tools you need, you’ll gain the confidence to negotiate like a pro.

Upsolve’s 5 Solid Steps for Negotiating With Debt Collectors article has more tips on how to negotiate with a debt collector like RMP Services.

How To Beat RMP Services in a Debt Lawsuit

Debt collectors typically don’t jump right to a lawsuit, but they do have the right to sue and may choose to do so if you ignore their collection efforts. If RMP Services does sue you, you will receive a summons and complaint, two official court documents notifying you of a lawsuit.

If a debt collector sues you, it’s important to respond quickly, or you may find yourself in worse trouble. Don’t worry, responding to a lawsuit is much easier than you may think.

If you're worried about responding on your own, but you can't afford a lawyer, you can draft an answer letter for free or a small fee using our partner Solo. They've helped hundreds of thousands of people respond to debt lawsuits, and they have a 100% money-back guarantee.

Solo is an affiliate partner, which means Upsolve may earn a small commission if you choose to use their paid service. This helps keep our services free.

Let’s look into our three-step response process together.

Step 1: Read the Summons and Complaint Carefully

A summons is a court document that alerts you to a lawsuit. The summons is especially important because it contains the basic information about your case, which you need when filling out your answer form (more on this below).

The information in a summons varies by court, but typically includes:

Your case number

The court name and address

Information on all parties involved

The nature of the lawsuit

The deadline for your response

Often, a complaint form is sent alongside your summons. The complaint lays out the plaintiff’s claims against you, usually in numbered paragraphs. The plaintiff is the company suing you. This information, as well as the details from your summons, helps you fill out your answer form.

Step 2: Fill Out an Answer Form (and Any Other Required Forms)

Now that you know the details of your lawsuit, you can move on to filling out your answer form. Some courts have answer form templates available, but not always. Check to see if your court provides one of these templates by Googling your court’s name and the phrase “answer form” or “court forms.”

If your court doesn’t have an answer form template, they may provide filing instructions and list any additional required forms on their website. See if your court has a “self-help” tab on their website. If you’re still unsure of the filing procedure, reach out to the court clerk. Clerks are court employees who can help you navigate any court procedure, including the answer form filing process. Keep in mind that they can’t give you legal advice about your case.

The answer form is your opportunity to state your “side” of the lawsuit and to bring up any defenses or affirmative defenses you have. Get more insight into defenses and how to handle a debt collection lawsuit in Upsolve’s article 3 Steps To Take if a Debt Collector Sues You.

Step 3: File the Answer Form With the Court and Serve on the Plaintiff

Check your summons or your court’s website to learn how to file your answer form. Most courts allow you to file in person or via mail. Some courts allow you to e-file or email your forms. You can always check with the court clerk if you aren’t sure about your options.

Most courts also require you to deliver a copy of your answer form to your collector. This is called serving the plaintiff. You can usually send your copy through the mail. When mailing any court documents, it’s advisable to use certified mail so you have proof the copy was sent.

Let’s Summarize…

If RMP Services claims you owe money, validate the debt first. If the debt is legitimate, figure out how much of the debt you can pay and how you want to pay. Then, you can start your debt settlement negotiations and settle for less than the original total amount. If RMP Services sues you, respond immediately by filing an answer form. You can still negotiate a debt settlement while navigating a lawsuit, just make sure you’re following all case requirements until the case is done and your settlement is finalized.