How To Answer an Alabama Debt Collection Court Summons

Upsolve is a nonprofit that helps erase your debt with our free bankruptcy filing tool. You could be debt-free in just 4 months. See if you qualify→

Upsolve is a nonprofit that erases your debt with our free bankruptcy filing tool. See if you qualify.

Answering a debt lawsuit is easier than you might think! You simply need to fill out an official court answer form, tell the court why you disagree with the lawsuit, and file the paperwork with the court. Then, you have to send a copy of your answer form to the person suing you. Finally, wait to get notice from the court about next steps. If you contest the lawsuit, the court will schedule a hearing date to hear both sides of the case.

Written by Ben Jackson. Legally reviewed by Jonathan Petts

Updated March 11, 2026

How Do Debt Collection Lawsuits in Alabama Work?

If you fall behind on a bill in Alabama, the company you owe may try to collect by calling or sending letters. Sometimes the original creditor handles this. Other times, they hire a collection agency or sell the debt to a debt buyer. If those efforts don’t work, the collector may file a lawsuit to collect the money.

🏛️ The court that handles the case depends on how much the collector says you owe. If the amount is $6,000 or less, the case usually goes to small claims court, which is part of Alabama’s district court. If the amount is more than $6,000 but no more than $20,000, the case is still filed in district court, just not on the small claims docket. Claims over $20,000 are typically filed in circuit court.

Many credit card and medical debt lawsuits involve a few thousand dollars, so they’re often filed in small claims or district court. This article focuses on what to expect in those cases.

How Do You Know if You’ve Been Sued for Debt in Alabama?

If a debt collector sues you, the court will send you official papers. These usually include a summons and a copy of the collector’s claims against you. In Alabama, the document that lists the claims is called a complaint or a statement of claim.

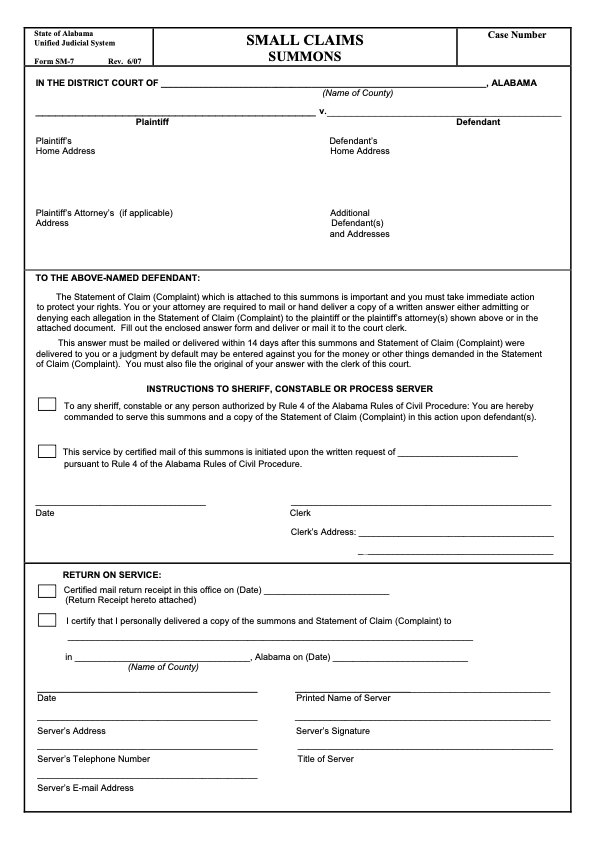

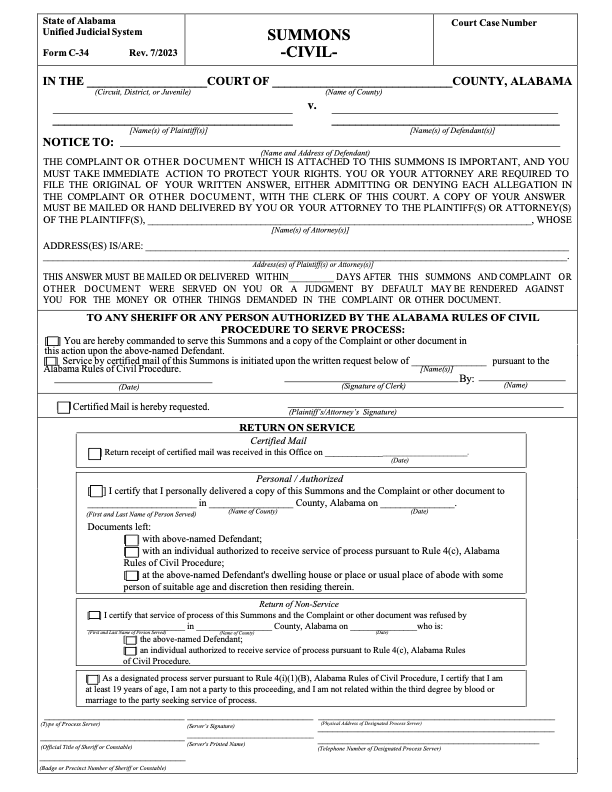

What Is a Court Summons?

📄 A summons is the court’s official notice that a lawsuit has been filed against you. It includes important information, such as:

The name of the court handling the case

The name and address of the plaintiff (the person or company suing you)

Your name and address as the defendant

The deadline to respond to the lawsuit

Here’s what a small claims summons form looks like:

If your case is filed in Alabama district court (outside of small claims), the civil summons will look similar to this:

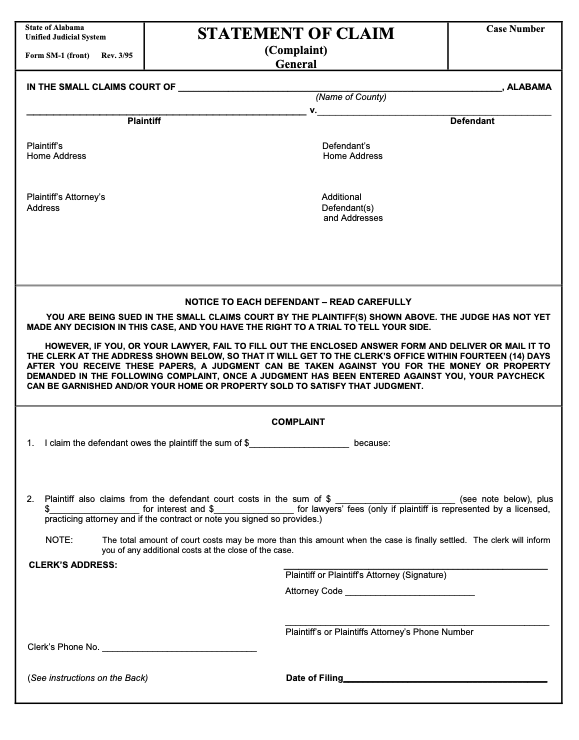

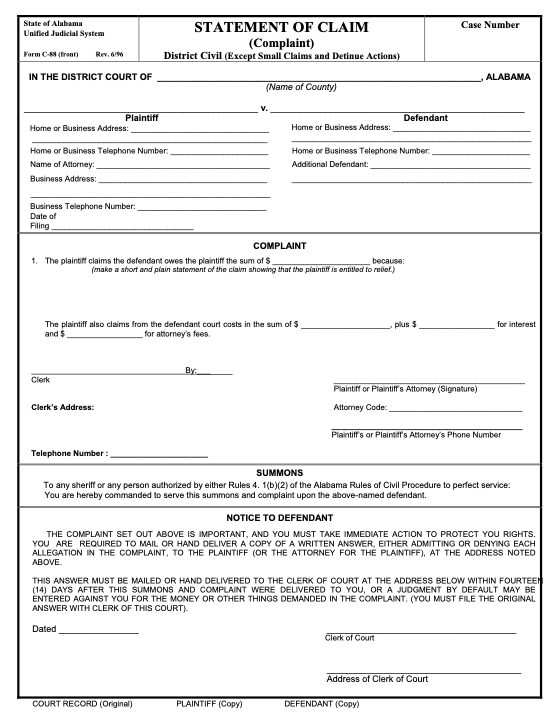

What Is a Statement of Claim?

The statement of claim (complaint) is the court document that explains why the plaintiff believes you owe money. It lists the amount they’re asking for, which may include the original debt, interest, court costs, and sometimes attorney fees.

🔍 Taking time to read this document carefully can help you decide whether you agree with the claims and whether anything looks inaccurate.

Here’s what a statement of claim for Alabama small claims court looks like:

If your case is filed in Alabama district court (outside of small claims), you’ll receive a statement of claim that looks like this:

How Long Do You Have To Respond to an Alabama Court Summons for Debt Collection?

⏳ Alabama doesn’t give you much time to reply to debt collection lawsuits filed in Alabama district court, including small claims cases. You have 14 days after you’re served with the court papers to respond by filing an answer with the court listed on the summons.

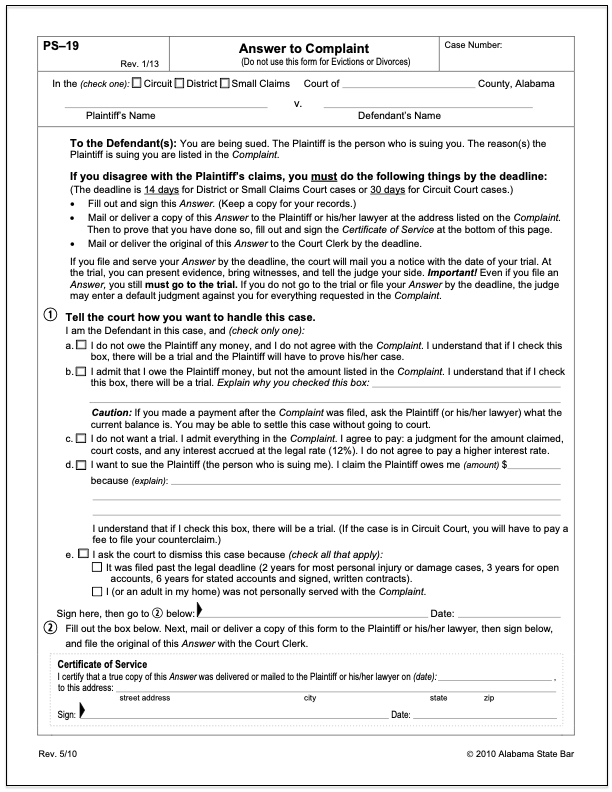

How Do You Fill Out an Answer Form for a Small Claims Case in Alabama?

To respond to a small claims lawsuit, you’ll need to complete a court-provided answer form. Many Alabama courts include a blank answer form with the summons and statement of claim. Sometimes parts of the form — such as the case number, court name, or clerk’s contact information — are already filled in. If they aren’t, you’ll need to add that information.

If an answer form isn’t included, you can usually download one from the court’s website. After you download the form, you can type your answers directly into the PDF or print it and fill it out by hand.

✨ If you're worried about responding on your own, but you can't afford a lawyer, you can draft an answer letter for a small fee using Solo. They've helped hundreds of thousands of people respond to debt lawsuits, and they have a 100% money-back guarantee.

Solo is an affiliate partner, which means Upsolve may earn a small commission if you choose to use their paid service. This helps keep our services free.

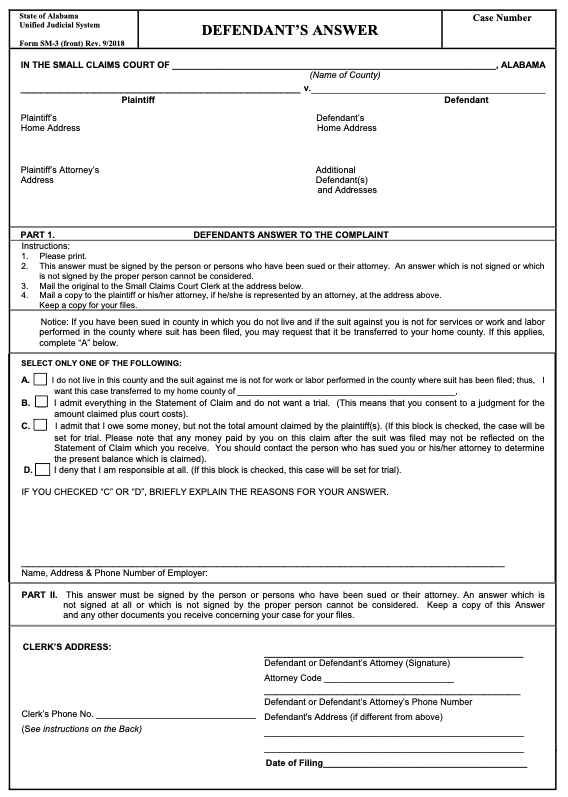

The small claims answer form is typically a one-page document with three main sections that looks like this:

After you download the form, you can type your answers directly into the PDF or you can print the form off and write your answers in by hand.

Step 1: Fill Out the Court Information

The top section of the form is usually straightforward if you have your summons and statement of claim nearby.

You’ll fill in:

The case number

The name of the county court hearing your case

The plaintiff's name and address

The defendant’s (your) name and address

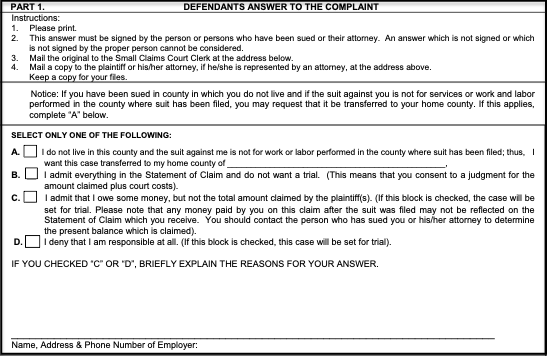

Step 2: Fill Out Part 1 of the Answer Form

The next section, Part 1, is where you respond to the lawsuit. Part 1 looks like this:

You’ll select one of four statements that best matches your situation:

Box A: The case was filed in the wrong county. This may apply if you don’t live or work in the county where the lawsuit was filed. Checking this box asks the court to move the case to a different county.

Box B: You agree you owe the debt and don’t plan to contest the lawsuit.

Box C: You believe you owe part of the debt, but not all of it.

Box D: You deny that you owe the debt.

If you choose C or D, the form includes space for a brief explanation. This is where you can state your defenses if you have them.

What Are Affirmative Defenses?

When you deny a lawsuit, you’re saying the collector’s claims aren’t true. For example, you might believe the amount is wrong or question whether the collector has the right to sue you. An affirmative defense is different. It’s a reason the collector shouldn’t win the case, even if some of the basic facts are accurate.

🛡️ Some common affirmative defenses in debt collection cases include:

The debt is past the statute of limitations. If your credit card or medical debt is more than six years old, it may be past the state’s statute of limitations. (Note that courts in Alabama have interpreted the statute of limitations for credit card debt differently. In some cases, it has been treated as three years.)

You already paid the debt. If that’s the case, proof of payment — like receipts or bank records — may support this affirmative defense.

The debt isn’t yours. When companies sell accounts to third-party collectors, they sometimes attach information to the wrong person.

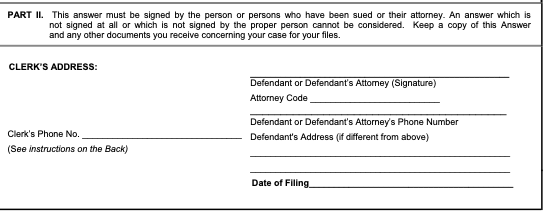

Step 3: Fill Out Part 2 of the Form and Make Copies

Part 2 is the signature section of the form. You’ll sign your name where it says “Defendant.” If the answer form came with your summons and statement of claim, the clerk’s contact information is often already filled in. That address tells you where to mail the completed form if you decide to file by mail.

📞 Keep the clerk’s phone number handy. If you have questions about what happens next or you need to reschedule future hearings, you can call the clerk.

📌 Once the form is complete, make at least one copy for your records. If your form includes a Certificate of Service section, follow the instructions on the form to send a copy to the plaintiff and complete that section before filing.

Step 4: File the Form With the Court

You can file your small claims answer form by mail or in person at the courthouse. Because you only have 14 days from the date you’re served to respond, it’s important to submit the form quickly. Filing in person can give you confirmation that the clerk received your answer.

📫 If you file by mail, the court advises you to call the clerk’s office a few days later to confirm your answer was received.

⚠️ If the court doesn’t receive your answer within 14 days, the court may rule in favor of the debt collector without hearing your side.

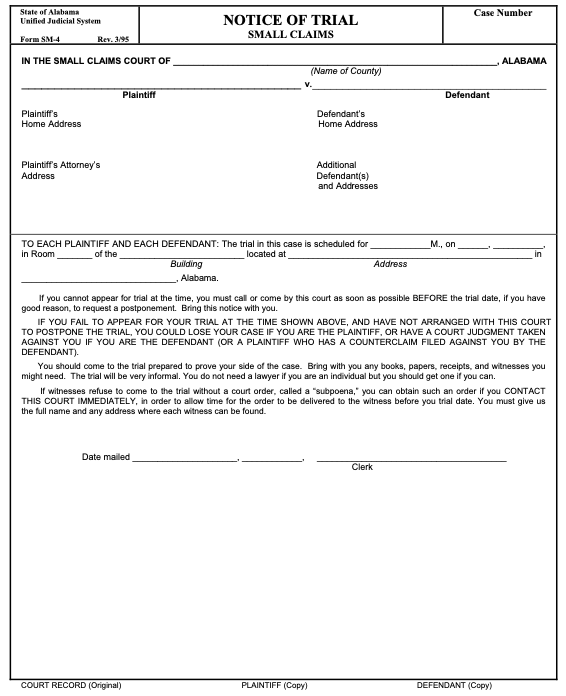

What Happens After You Respond to the Lawsuit?

After you file your answer, the court will send you a notice of trial. This notice lists the trial date, time, and location. It also explains what to expect and warns that the court may decide the case without you if you don’t appear.

The notice of trial looks like this:

📂 Before your trial date, take time to review your case and organize any documents related to the debt. In debt collection cases, the plaintiff must show that they own the debt and have the legal right to collect it. If you plan to dispute the claim, you may want to bring records, such as payment receipts, bank or credit card statements, or notes from conversations with the debt collector.

How Do You Fill Out an Answer Form for Debt Lawsuits in an Alabama District Court?

If your case is filed in Alabama district court but not on the small claims docket, the process for responding is similar. However, the forms and deadlines may be slightly different.

In these cases, you may not receive a blank answer form with your summons and complaint. You can download the form from the court’s website if one isn’t included. Depending on your county, you may also have the option to e-file your answer.

The district court answer form looks like this:

As shown on the form, you’ll start by filling in the court and case information at the top. Then select the lettered option that best fits your response:

Box A: You don’t believe you owe the plaintiff any money and would like them to prove their case.

Box B: You admit you owe some money, but they got the amount wrong.

Box C: You admit you owe the amount listed in the complaint and agree to pay it, including any accrued interest.

Box D: You are filing a counterclaim against the plaintiff.

Box E: You are asking the court to dismiss the case. This may apply if:

The debt is past the statute of limitations.

The plaintiff didn’t properly serve the complaint.

If the form asks for additional details, provide a brief explanation in the space provided.

Once the form is complete, make two copies. Mail or deliver one copy to the plaintiff or the plaintiff’s attorney at the address listed on the summons. Then complete the Certificate of Service section on the form to show that you’ve sent it.

After that, file the original with the court — electronically (if available in your county), by mail, or in person. Keep the remaining copy for your records.

What Happens if You Don’t Respond to the Lawsuit?

Facing a debt collection lawsuit can feel overwhelming, but responding is often easier than people expect. And it’s worth doing. If you don’t respond, the court may enter a default judgment against you. A default judgment can allow the debt collector to collect the money through wage garnishment or a bank levy.

Debt collectors know that many people don’t respond. When no answer is filed, they can win without proving their case. Filing an answer changes that by requiring the collector to show they have the legal right to collect the debt.

🤝 You can still try to settle the debt after you’re served with a summons. That’s common. Unless the case has been officially resolved, court deadlines still apply. It’s important to still file your answer on time and appear at scheduled court dates while settlement talks are ongoing.

What if There’s Already a Default Judgment Against You?

If a default judgment has already been entered against you, you may still have options. In some situations, you can file a motion to vacate, which asks the court to cancel the judgment and reopen the case so you can respond to the lawsuit.

This process is often more complicated than filing an answer and may involve strict deadlines. If you want to explore this option, contact the court clerk to ask about the required forms and whether a deadline applies. The clerk can’t give legal advice, but they can explain the court’s procedures.

Need Legal Help?

If you’d like extra support, there are free and low-cost legal resources available in Alabama. The organizations below may be able to help:

Legal Services Alabama provides free or low-cost legal help for qualified individuals.

The Alabama State Law Library has resources for individuals representing themselves in court.

The Alabama State Bar lists legal clinics, which are programs that offer free or low-cost legal services, advice, and representation to individuals.