How To Answer an Oregon Debt Collection Court Summons

Upsolve is a nonprofit that helps erase your debt with our free bankruptcy filing tool. You could be debt-free in just 4 months. See if you qualify→

Upsolve is a nonprofit that erases your debt with our free bankruptcy filing tool. See if you qualify.

If you’re sued for a debt in Oregon, you’ll receive an official notice from the court. If you’re sued in small claims court, you need to respond to the notice and tell the court if you want a hearing or jury trial. If you’re sued in regular circuit court, you need to respond with an answer form that includes any affirmative defenses you may have. After responding in either situation, you must show up to required court appearances, which could be a hearing, mediation, or arbitration, depending on your case.

Written by Attorney Tina Tran. Legally reviewed by Jonathan Petts

Updated March 10, 2026

How Do Debt Collection Lawsuits in Oregon Work?

If you fall behind on your bills, a creditor may send your account to a debt collector. At first, you may get phone calls and collection letters. If the debt remains unpaid, the collector may file a lawsuit.

In Oregon, debt collection lawsuits can be filed in either circuit court or justice court. Circuit courts can hear civil cases involving any dollar amount. Justice courts can hear civil cases where the amount claimed is $10,000 or less.

⚖️ Both courts handle cases in one of two ways:

Through the small claims department, which uses a simpler and faster process

Through the court’s regular civil process, which is more formal

What matters most isn’t which court filed the case — it’s whether your case is being handled in small claims or as a regular civil case. The paperwork you receive will tell you which process applies.

How Do You Know You’ve Been Sued?

If a debt collector files a lawsuit against you, you’ll receive official court paperwork. The documents you receive will show whether your case is in small claims or being handled through the regular civil process.

No matter which type of case it is, the paperwork will include important details, such as:

How to respond

How long you have to respond (usually 30 days)

What could happen if you don’t respond

If the case was filed in small claims, you’ll receive a form called a Small Claim and Notice of Small Claim.

👇 The first page of the small claims form usually looks like this:

If the case was filed as a regular civil case, you’ll receive two documents: a summons and a complaint.

The summons will say “Summons” at the top. It lists the plaintiff (the person or company suing you), your name as the defendant, and the name of the court. It explains that you’re being sued and tells you how long you have to respond.

The complaint explains why the plaintiff says you owe the debt. It usually includes numbered paragraphs describing the account, how much they claim you owe, and how the debt began or was assigned to them. It also explains what they’re asking the court to do. In most cases, they’re asking for a money judgment for the amount claimed, plus court costs and possibly attorney fees.

How Do You Respond to an Oregon Small Claims Notice?

If you receive a Small Claim and Notice of Small Claim, you generally have 30 days to respond. If you don’t respond within that time, the court may enter a default judgment against you. That means the plaintiff could win automatically.

📝 To respond, you’ll complete a Defendant’s Response form. This form lets you tell the court how you want to move forward. You can:

Pay the claim and show proof of payment.

Deny the claim and request a hearing.

Deny the claim and request a jury trial (if the total amount claimed is more than $750).

File a counterclaim if you believe the plaintiff owes you money related to the same dispute.

💻 Oregon Judicial Department (OJD) iForms is an online tool that helps people prepare court forms. You can use it to fill out your response online. You can also print out the form and complete it by hand.

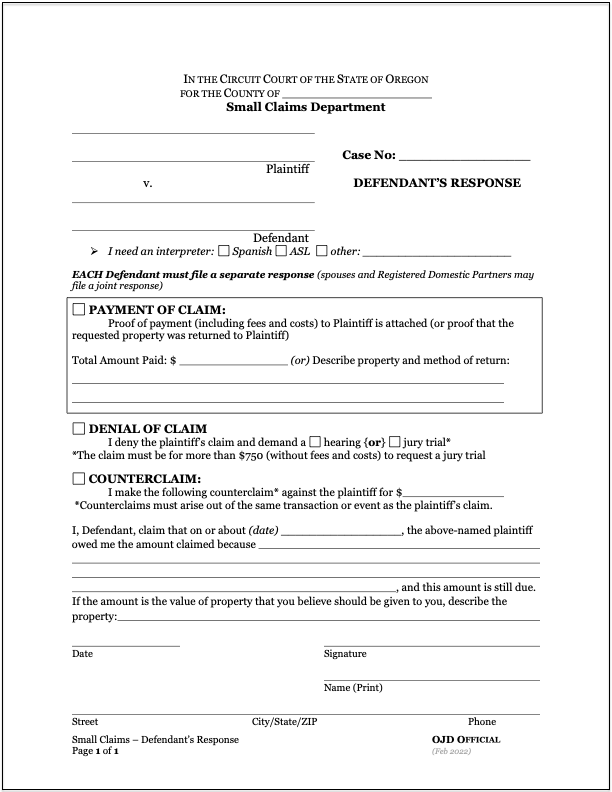

Here’s what the form looks like:

Step 1: Fill in the Case Information

Use your Small Claim and Notice of Small Claim form for reference to complete the top section of the Defendant’s Response. You’ll fill in:

The county name

The plaintiff’s name

Your name as the defendant

The case number

If you need an interpreter, you can check the appropriate box on the form to let the court know.

Step 2: Address the Claim

Next, you’ll see three main options:

Payment of Claim

Denial of Claim

Counterclaim

If you’ve already paid the claim in full, you can check “Payment of Claim” and attach proof of payment.

If you disagree with the claim, check “Denial of Claim.” The form will then ask whether you want:

A hearing: A hearing is decided by a judge. Both you and the plaintiff appear and explain your sides of the story. If you choose this option, the court will schedule a hearing date and send you notice.

A jury trial: A jury trial is decided by a jury instead of a judge. It follows a more formal process and may involve additional fees. You can request a jury trial only if the total amount claimed (including interest, fees, and costs) is more than $750.

If you believe the plaintiff owes you money related to the same dispute, you can check “Counterclaim.” The form includes space to explain your claim. Counterclaims must arise out of the same transaction or event as the plaintiff’s claim. Counterclaims follow additional rules and procedures.

🔍 If you’re unsure which option fits your situation, review the court’s instructions to help you understand the differences.

Step 3: File Your Response With the Court

After you complete the Defendant’s Response form, file it with the court listed on your Small Claim notice and include the required response fee. You can find current fee information on the Oregon Judicial Department website.

If you can’t afford the fee, you may be able to ask the court for a fee waiver or deferral. Be sure to keep a copy of your filed response for your records.

Step 4: Attend Mediation and/or the Hearing

After you file your response, the court will notify you of the date, time, and location of your next required appearance. This is usually mediation or a hearing and may take place in person or remotely. Be sure to attend any scheduled court dates.

In some Oregon courts, small claims cases are referred to mediation before a hearing. Mediation is a meeting with a trained, neutral third party who helps both sides try to resolve the case without going to trial. Whether mediation is required depends on the court’s local rules. If the case isn’t resolved in mediation, the court will schedule a hearing (trial).

📂 Small claims court is designed for people without lawyers. Hearings are more informal than regular civil court trials, but you should still come prepared. Bring any documents or other evidence that supports your position, such as contracts, account statements, receipts, or proof of payment.

🗣️ At the hearing, the plaintiff usually presents their side first. Then you’ll have a chance to explain your position and present your evidence. Speak respectfully to the judge and others in the courtroom. Address the judge as “Your Honor,” and arrive on time.

How Do You Respond to a Debt Lawsuit in Civil Court?

If you receive a summons and complaint, you must respond by filing an answer with the court. Oregon doesn’t provide a standard statewide answer form for regular civil cases, but you can use a template like this one from Columbia County as a guide.

Your answer should include the name of the court, the names of the parties, the case number, and a title that clearly says “Answer.”

📝 In your answer, you’ll need to:

Respond to each numbered paragraph in the complaint by stating whether you admit, deny, or don’t have enough information to admit or deny the claim.

List any affirmative defenses you are raising.

Include a certificate of service showing that you sent a copy of your answer to the plaintiff or the plaintiff’s attorney.

Regular civil cases follow formal court rules, so review the summons carefully and follow its instructions for filing and serving your response.

✨ If you're worried about responding on your own, but you can't afford a lawyer, you can draft an answer letter for a small fee using Solo. They've helped hundreds of thousands of people respond to debt lawsuits, and they have a 100% money-back guarantee.

Solo is an affiliate partner, which means Upsolve may earn a small commission if you choose to use their paid service. This helps keep our services free.

Step 1: Address Each Statement in the Complaint

As mentioned above, your answer must respond to every numbered statement in the complaint. For each paragraph, include the paragraph number and one of the following responses:

Admit: You agree that the statement is true.

Deny: You disagree with the statement or believe it is not true.

Lack sufficient information to admit or deny: You don’t know whether the statement is true, either because the complaint does not provide enough information or because the claim involves something outside your knowledge (for example, the plaintiff’s internal business records).

⚠️ If you don’t respond to a paragraph, the court may treat it as admitted.

Step 2: Raise Your Defenses

Defenses are legal reasons the plaintiff shouldn’t win the case. Sometimes a defense points out a mistake in the complaint or a lack of proof. Even if the complaint’s facts are mostly correct, you may still have an affirmative defense — a legal reason the court shouldn’t enter judgment against you.

🛡️ Here are some common affirmative defenses in debt collection cases:

Expired statute of limitations: The lawsuit was filed after the legal deadline to collect the debt.

Lack of standing: The plaintiff can’t prove they have the legal right to sue you for the debt.

Improper service: You weren’t properly served with the lawsuit papers.

Prior payment: You already paid all or part of the debt.

Identity theft or fraud: The debt resulted from identity theft or fraudulent activity.

Prior settlement or agreement: The debt was resolved or modified through a prior agreement.

Unlawful debt collection practices: The debt collector violated state or federal debt collection laws, including special protections that apply to certain debts, such as medical debt.

Failure to include required debt buyer disclosures: In some cases involving debt buyers, Oregon law requires the complaint to include a Consumer Debt Collection Disclosure form. If required disclosures weren’t included, that may be something you can raise as a defense.

👉 If you believe any of these apply to your case, you can include them as affirmative defenses in your answer. If possible, gather documents or other evidence that supports your defense, such as account statements, receipts, proof of payment, police reports (for identity theft), or written agreements.

Step 3: File Your Forms With the Court Clerk and Serve the Plaintiff

Once you’ve finished your answer, the next step is to file it with the court and send a copy to the plaintiff.

💻 Many Oregon courts allow you to e-file your paperwork. It’s often the quickest way to submit your documents, so check with your court to see if that option is available.

If you’re filing by mail or in person, make at least two copies of your completed answer. File the original with the court listed on your summons. Then mail one copy to the plaintiff or their attorney (their contact information is on the summons). Keep the extra copy for your records.

You must include a certificate of service stating when and how you sent a copy of your answer. Oregon courts provide a general Certificate of Service form you can use.

If you’re mailing your documents, consider using certified mail so you have proof they were sent.

What Happens After You Respond to the Lawsuit?

If your case is in regular civil court and the amount claimed is $50,000 or less, it will likely go to mandatory arbitration instead of a trial. Arbitration is less formal than court. Instead of a judge or jury, a neutral arbitrator — usually an experienced lawyer or retired judge — hears both sides, reviews the evidence, and makes a decision.

🔄️ Before this happens, you and the plaintiff may need to exchange evidence. During the arbitration session, each side explains their position and presents documents or witnesses. After the hearing, the arbitrator issues a written decision called an award.

If no one objects within 20 days, the award becomes a court judgment. If the losing side objects in time, they can request a new trial in court.

No matter what stage your case is in, come prepared. Bring your documents, know your defenses, and be ready to clearly explain your side.

What Happens if You Don’t Respond to the Lawsuit?

If you don’t respond to the lawsuit, the court will likely enter a default judgment against you. A default judgment means you automatically lose the case because you didn’t file a response. Once that happens, the creditor may be able to take additional collection actions, such as wage garnishment or a bank levy.

The good news is that you can prevent this simply by responding. Filing a response or answer gives you the chance to raise defenses and require the creditor to prove their case. In some situations, that can even lead to the case being dismissed.

If a default judgment has already been entered, you may still have options. In some situations, you can ask the court to cancel (vacate) the judgment by filing a motion. To learn more, read our article How Do You Cancel (Vacate) a Court Judgment?

Need Legal Help?

If you’re feeling unsure about handling your case on your own, free and low-cost legal help is available in Oregon. Here are some places to start:

Legal Aid Services of Oregon provides free or low-cost legal help to qualifying individuals.

Oregon Law Help can help you find legal aid services and other legal help near you.

Oregon has a legal referral program that connects people with low-cost legal assistance.