How To Win Against Frost-Arnett Company

Upsolve is a nonprofit that helps erase your debt with our free bankruptcy filing tool. You could be debt-free in just 4 months. See if you qualify→

Upsolve is a nonprofit that erases your debt with our free bankruptcy filing tool. See if you qualify.

Frost-Arnett is a debt collection agency. If Frost-Arnett contacts you, they’re probably trying to collect a past-due medical debt on behalf of a healthcare company they bought the debt from. If the debt is legitimate, you likely have to pay or face serious consequences. But don’t fret! You may not have to pay the full amount. You can try to negotiate a debt settlement to pay a portion of the debt and settle the account for good. If Frost-Arnett repeatedly contacts you and you ignore them, they could file a lawsuit against you. Respond to the lawsuit right away by filing an answer form with your court.

Written by the Upsolve Team. Legally reviewed by Jonathan Petts

Updated March 12, 2026

Why Is Frost-Arnett Contacting Me?

Frost-Arnett is a debt collection agency that collects past-due debts for healthcare companies. If they are contacting you, you may owe money to a medical provider.

Read Upsolve’s article on How To Deal With Frost-Arnett to learn more about how they operate and what to do if they contact you.

Do I Have To Pay Frost-Arnett?

You might have to pay Frost-Arnett. It depends on whether they can prove the debt is valid.

If they can’t validate the debt or you think the amount is wrong, you can dispute the debt.

If they can validate the debt and you agree you owe the amount they’re asking for, you should pay to avoid serious consequences. For example, Frost-Arnett can get a court order to freeze your bank account or garnish your wages. However, you may not have to pay the whole debt. If you can’t afford to pay off the full amount, try negotiating the debt down.

How To Negotiate a Debt Settlement With Frost-Arnett in 3 Steps

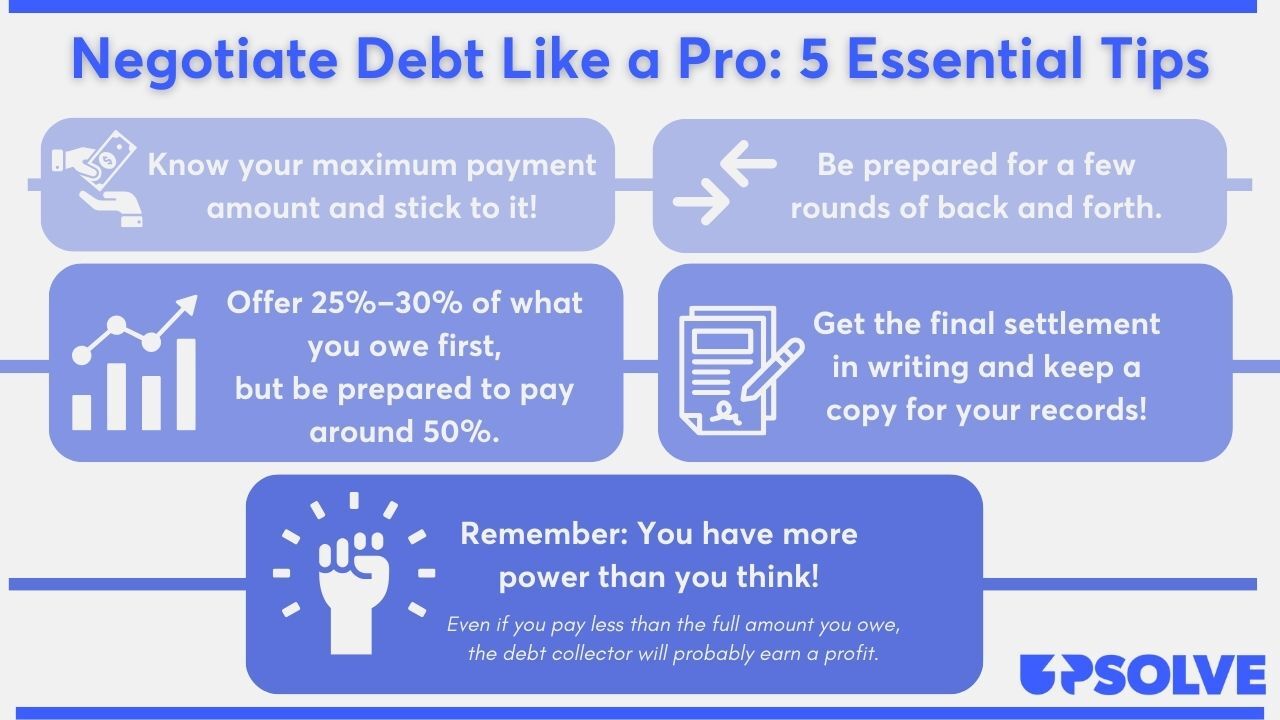

Debt collection is a profitable business. Typically, debt collectors like Frost-Arnett buy charged-off debt accounts for much less than they’re worth, or they may earn a small percentage of each debt account they collect successfully. They need to make money to keep their business afloat, which means you have a surprising edge when it comes to debt settlement negotiations.

Even if they settle with you for 40%–60% of the original amount (which most collectors will), they can still profit. In fact, this is often a win-win: You get to pay an amount you can afford, the debt collector gets paid, and the account is closed for good.

If Frost-Arnett doesn’t reach out to offer a settlement or begin negotiations, there’s no reason why you can’t get the ball rolling. By starting the conversation, you have more control over how the settlement proceeds. Don’t worry, it’s not as scary as you may think! Let’s go through the negotiation process together.

Step 1: Make Sure the Debt Is Valid

If Frost-Arnett hasn’t sent you a debt validation letter, ask for one immediately. Third-party debt collectors have to send you a debt validation letter and give you 30 days to dispute the debt, according to a debt collection rule created by the Consumer Financial Protection Bureau (CFPB).

The validation letter should help you verify that:

The debt account really belongs to you

Frost-Arnett legitimately owns or has the legal right to collect the debt

The debt amount is right

If the validation letter doesn’t contain enough information for you to verify the debt, you can craft and send a debt verification letter. This letter can also be used to dispute the debt.

Once you confirm the debt is legitimate and belongs to you, you can figure out how much of the debt you can pay and make your debt settlement offer.

Step 2: Figure Out What You Can Pay

To figure out how much of the debt you can comfortably pay, take a look at your take-home pay and monthly expenses. The CFPB has a debt worksheet that can help you organize your bills (monthly car payments, credit card bills, housing payment, etc.) and a budgeting worksheet that can help you craft your new budget.

We know that taking a close look at your finances can be daunting. If you need a little extra help, inquire about a free consultation with a local accredited nonprofit credit counselor.

Lump-Sum Payment vs Payment Plan: Which Is Better?

You can repay your debt to Frost-Arnett in one of two ways: a lump-sum payment or a payment plan. Deciding which option to go with depends on your financial situation.

Debt collectors typically prefer lump-sum payments because it gives them the most money upfront. If you’re expecting a bump in income, like a bonus from work or a tax return, consider using it to pay one lump sum. The biggest advantage of offering a lump-sum payment is that you can usually negotiate a lower repayment amount if you can offer the money quickly.

If you’re not expecting additional income soon and don’t have extra money in savings, a payment plan might be the better option for you. If so, offer a monthly payment amount and a payment timeline you feel confident you can stick to. If you can, offer to set up a direct bank account withdrawal for the monthly payments. This can boost your chances of Frost-Arnett accepting your payment plan settlement offer, and it may help you negotiate a lower repayment amount.

Step 3: Make a Settlement Offer to Frost-Arnett

Now that you know how much of the debt you can pay and how you’ll pay it, it’s time to make a settlement offer. You can make this offer in writing using Upsolve’s Debt Settlement Letter template, but it’s usually best to call the debt collector up and speak to them directly. Always ask for written confirmation of any important information Frost-Arnett tells you over the phone.

How Do Medical Bills Affect Your Credit Score?

If you have a medical debt sent to collections, check your credit report. You can get a free credit report every week from AnnualCreditReport.com. Many medical debts should not appear on your credit report or affect your credit score, including:

Medical collections accounts under $500

Paid medical collections accounts

Medical collections accounts that are less than one year old

If any of these appear on your credit report, you can dispute them to have them removed. Doing so will probably help boost your credit score.

Can You Still Negotiate a Settlement if There’s a Debt Lawsuit Against You?

Often, yes. You can probably still negotiate a settlement even if you’re in the middle of a debt lawsuit. If you want to go this route, however, you still need to actively participate in your lawsuit. Continue showing up to appearances and following court requirements until your settlement is complete or your lawsuit is closed or dismissed.

Tips for a Successful Debt Settlement

Most people are nervous about negotiating with a debt collector, which is completely understandable! It can feel intimidating, but once you know our tips on negotiating like a pro, you’ll feel ready to take on Frost-Arnett.

Upsolve’s article 5 Solid Steps for Negotiating With Debt Collectors has even more tips on how to negotiate with a debt collector like Frost-Arnett.

How To Beat Frost-Arnett in a Debt Lawsuit

It’s uncommon for Frost-Arnett to sue, but they do have a right to file a lawsuit against you. If they do sue you, you will receive official court documents called a summons and complaint.

Responding to a lawsuit is vital. If you do not respond to a debt collector after they file a lawsuit against you, they could get a default judgment to garnish your wages or your bank account. Don’t worry, responding to a lawsuit is easier than you may think!

If you're worried about responding on your own, but you can't afford a lawyer, you can draft an answer letter for free or a small fee using our partner Solo. They've helped hundreds of thousands of people respond to debt lawsuits, and they have a 100% money-back guarantee.

Solo is an affiliate partner, which means Upsolve may earn a small commission if you choose to use their paid service. This helps keep our services free.

Step 1: Read the Summons and Complaint Carefully

A summons is a document that notifies you of a lawsuit. It lets you know someone — in this case, the debt collector — is suing you and “summons” you to court. Your summons will have important information you need to fill out your answer form (more on this below).

Your summons will usually include:

The court’s name and address

Your case number

Details on all parties involved (and their contact information)

Instruction for answering your summons

The legal consequences if you don’t respond to the lawsuit

Summons forms may vary depending on your court, as will complaint forms. A complaint form is a document that outlines the specific claims the debt collector has made against you, often in numbered paragraphs.

Step 2: Fill Out an Answer Form (and Any Other Required Forms)

Many, but not all, courts have blank answer form templates on their websites. Google the court’s name on the summons and “answer form” or “court forms” to check if your court provides one of these templates.

The answer form is your response to the lawsuit and your opportunity to state specific reasons — called defenses or “affirmative defenses” — why Frost-Arnett should not win the lawsuit. Upsolve’s article 3 Steps To Take if a Debt Collector Sues You can provide further guidance on handling a debt collection lawsuit.

If you’re confused about your court’s process or can’t find a required form, like an answer form or a certificate of service, you can always contact your court clerk. A court clerk is a court official who can help you with your paperwork and the court’s proceedings, but they cannot give any legal advice.

Once you have your paperwork filled out, you’re ready to file your answer form with your court.

Step 3: File the Answer Form With the Court and Serve on the Plaintiff

The last steps in this process are to file your answer form with your court and deliver a copy of your paperwork to the plaintiff (Frost-Arnett or the lawyer representing them). Like most court procedures, the filing process differs depending on your court.

Most courts allow you to file the form in person or by mail. Some allow you to e-file the form online. Check your court’s rules or with the court clerk to learn your options. Most courts require you to deliver a copy of your form to Frost-Arnett. You can usually do this through the mail.

Let’s Summarize…

If Frost-Arnett contacts you about a debt you owe to a healthcare provider, verify the debt. If it’s valid, you can resolve the debt by negotiating a debt settlement. This way, you settle the debt but you don’t have to pay the entire amount. Go into your negotiations prepared and confident, and be ready for some back and forth. If Frost-Arnett files a lawsuit against you, it’s not too late to negotiate a settlement, but you need to make sure you’re following through with all lawsuit requirements until the case is closed or the settlement is in writing.