How To Deal With Halsted Financial Services

Upsolve is a nonprofit that helps erase your debt with our free bankruptcy filing tool. You could be debt-free in just 4 months. See if you qualify→

Upsolve is a nonprofit that erases your debt with our free bankruptcy filing tool. See if you qualify.

Halsted Financial Services is a debt collection agency with a primary focus on past-due consumer debts, such as personal loans, credit cards, and medical bills. If Halsted Financial Services calls you or sends you letters to collect a debt, ask them to validate the debt. This article explains how to verify a debt and explores your options, such as contesting the debt, negotiating a debt settlement, or ignoring the debt (not advised). There’s also information on how to deal with a debt collection lawsuit.

Written by Mae Koppes. Legally reviewed by Jonathan Petts

Updated March 14, 2026

What Is Halsted Financial Services?

Halsted Financial Services LLC, based in Skokie, Illinois, is a third-party debt collector with clients that include healthcare providers, credit card companies, and payday loan providers.

Halsted primarily collects past-due accounts on behalf of creditors and lenders.

Why Is Halsted Financial Services Contacting Me?

If Halsted contacts you, you may have an unpaid debt with an original creditor.

Halsted operates differently than most debt collection agencies. Most debt collectors buy charged-off debts from original creditors and try to collect the debts for their own profit. Instead, Halsted usually collects debts on behalf of original creditors, earning a percentage of each collected debt account. Halsted encourages the consumers they contact to pay them directly using their online payment system.

If Halsted Financial Services has contacted you but you're unsure of the debt's origin or the original creditor, you can call them at (855) 284-0831 to request additional information.

Is Halsted Financial Services Legit?

Yes, Halsted Financial Services is a legitimate debt collector. Halsted is accredited with the Better Business Bureau (BBB), which currently gives the company a B grade. The company’s customer rating is considerably better than most other collection agencies. Customers rate it 4.67 out of 5 stars, with more than 320 reviews.

Despite this rating, more than 350 consumer complaints were filed against Halsted in the past three years, while the Consumer Financial Protection Bureau’s (CFPB) Consumer Complaint Database received more than 650 complaints since December 2011.

Note to reader: These reviews and complaints highlight relevant issues, but they may not represent all consumers’ experiences.

Know Your Rights!

Consumer complaints against Halsted Financial Services allege improper disclosure of debt information to others, trying to collect a debt not owed, threatening jail for not paying a debt, and impersonating law enforcement.

A debt collector making these statements or taking these actions could be in violation of the Fair Debt Collection Practices Act (FDCPA). This federal law prohibits third-party debt collectors from harassing consumers or making misleading and threatening statements.

Under the FDCPA, you have the right to:

Ask for debt validation in writing within 30 days of the first contact.

Tell a debt collector to stop contacting you, and they must stop (except to confirm they’re stopping or taking legal action).

Dispute the debt if you believe it’s incorrect or doesn’t belong to you.

Be free from harassment, including repeated calls, threats, or abusive language.

Limit when and how you’re contacted, such as no calls before 8 a.m., after 9 p.m., or at work if you ask them not to.

Keep your personal information private — collectors can’t discuss your debt with anyone other than you, your spouse, or your attorney.

If you feel your rights have been violated, you can:

File a complaint with the Consumer Financial Protection Bureau (CFPB) or your state attorney general.

Send a cease-and-desist letter to the collector.

Consider talking to a consumer protection attorney, especially if you’ve suffered financial or emotional harm as a result of the violation.

How Do I Know if I’m Being Scammed?

Though Halsted Financial Services is a legitimate company, fraudsters can use real company names to trick people into sharing personal information or sending money.

To avoid being the victim of identity theft, ask anyone trying to collect a debt from you to validate the debt. Even better, if you think you’re on the phone with a scammer, hang up. The longer you talk to them, the more opportunities they have to convince you to give personal information or send money.

To learn more about debt collector scams, read Upsolve’s article How To Avoid Debt Collector Scams: 8 Red Flags.

Do I Have To Pay Halsted Financial Services?

You might need to pay the debt, but you should first confirm there isn’t a mistake or mix-up. When creditors partner with third-party agencies to collect debt, errors can happen. For example, debt collectors may try to collect a debt that’s already been paid or belongs to someone else. This is why it’s important to validate that Halsted can collect the debt from you and that the amount is correct.

If Halsted can’t prove the debt is yours, then you don’t have to pay them and they should stop contacting you if you tell them in writing to stop.

If they can prove it’s yours and they own it, you have to decide what to do next.

Step 1: Send a Debt Verification Letter

Within five days of contacting you for the first time, Halsted should send you a debt validation letter (sometimes called a validation notice). If they don’t, you can send them a debt verification letter. The purpose of these letters is to obtain more information about the debt to confirm it’s valid.

In addition to information about the debt account, the validation letter should contain information about how to dispute the debt if you disagree with it. Read your validation letter carefully for information about the 30-day deadline for disputing the debt. If you decide to dispute the debt within these 30 days, Halsted must cease collection activity until the dispute is resolved.If Halsted can’t verify the debt, you don’t need to pay the debt and you can tell them to stop contacting you. In this situation, it’s a good idea to check your credit report and credit score for any errors.

If Halsted can verify the debt, you must decide what to do next.

Step 2: Decide What To Do Next

Though this can be stressful, remember that you have options. You can dispute the debt or try to settle the debt for less than what you owe. Ignoring the debt is not recommended.

✨ If this is just one of many overwhelming debts, it might be time to consider getting a full financial reset by filing Chapter 7. Upsolve's free filing tool can help people with simple cases file for free.

Option 1: Dispute the Debt

If Halsted has validated the debt but you disagree with the amount or don’t believe the debt is yours, you can dispute it.

At this point, double-check your credit report for errors. If you see a mistake on your credit report, contact the credit bureau (TransUnion, Experian, or Equifax) reporting it and ask them to remove the error from your credit report by sending a credit dispute letter.

The Fair Credit Reporting Act (FCRA) gives consumers the right to dispute errors on their credit reports.

Option 2: Negotiate the Debt and Make a Settlement Offer

Halsted is often willing to settle a debt for less than the full amount. Debt collectors like Halsted only get paid if you pay them, and they know you may not be in a financial position to pay off the debt completely.

Remember, they want to close collection accounts, so they have an incentive to work with you to make it happen, even if it means they earn less.

Learn more in the “How To Negotiate a Debt Settlement With Halsted Financial Services in 3 Steps” section below.

What Happens if I Ignore Halsted Financial Services?

Ignoring Halsted can come with serious negative consequences, including:

More debt due to interest, fees, and legal costs

A lower credit score

A possible lawsuit, which can result in a court order for wage garnishment

Continued debt collection efforts — debt collectors rarely give up when ignored

Ignoring debt collectors is never a good idea. Debt collectors can still take legal action against you as long as the statute of limitations hasn’t passed. Even if it has, a debt collector might still try to sue you or continue debt collection attempts, like phone calls and letters.

This doesn’t sound like the most encouraging news, but keep your head up. Knowledge is power.

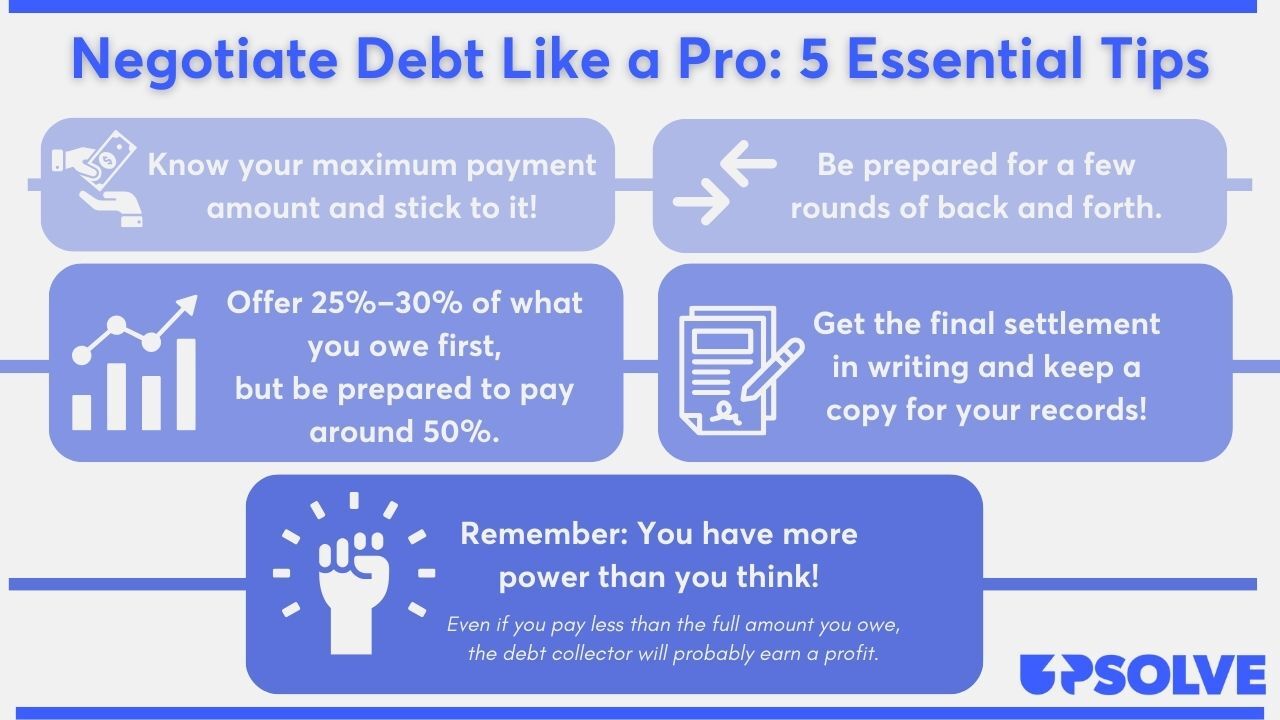

How To Negotiate a Debt Settlement With Halsted Financial Services in 3 Steps

Navigating debt negotiations with Halsted Financial Services might feel daunting, but understanding the dynamics of debt collection can work in your favor and empower you to take action.

You can start a debt negotiation by writing a debt settlement letter. Many people make an initial offer of 25% or 30% of the original debt amount. Expect some back and forth, though. It’s common to agree on something around 50% or 60%.

Many debt collectors are open to settling for 40% to 60% of the original debt. While debt collectors sometimes initiate settlement offers, you can start the conversation to get the ball rolling.

The good news is, once you understand the basics, negotiating your debt is easier than you might think. Start by making sure the debt is valid.

Step 1: Make Sure the Debt Is Valid

Third-party debt collectors like Halsted must send you a debt validation letter (also known as a validation notice) that gives you details of the debt account within five days of contacting you.

This is required under a Consumer Financial Protection Bureau (CFPB) debt collection rule. The rule also states that the debt collector has to notify you of your right to dispute the debt and give you 30 days to do so.

If you haven’t received a debt validation letter, ask for one. Then read it carefully to make sure that:

The debt belongs to you.

Halsted Financial Services is legally allowed to collect the debt.

The debt amount on the letter is correct.

Unfortunately, sometimes people learn they are victims of identity theft or that the creditor simply has the wrong account holder. Mistakes happen, so ask questions!

If you need more details about the debt account or if the information on the validation letter appears incorrect, you can write a debt verification letter. Here’s the difference between a validation and verification letter:

Step 2: Figure Out What You Can Pay

Once you confirm that the debt is yours and the amount is correct, it’s time to figure out how much you can pay. Review your monthly income and expenses to figure out how much you could put toward your debt repayment. It may help to create a budget to see how your expenses and other debt payments compare to your income. The goal is to determine a realistic payment amount for yourself.

If you need help with this process, consider a free consultation with an accredited nonprofit credit counselor.

Lump Sum vs. Monthly Payments: Which Is Better?

If you can make a lump-sum payment rather than setting up a monthly payment plan, your settlement offer is more likely to be accepted, and you may be able to negotiate a lower amount. Are you expecting a potential work bonus, tax refund, or some other financial windfall? If so, consider using it to make a lump-sum payment.

If a payment plan is your only option, make sure that the amount you commit to monthly fits your budget. And be sure it also allows you to continue to cover your basic expenses like food and housing without stress. Some companies may be more willing to agree to a payment plan if you authorize direct withdrawal from your bank account.

Step 3: Make a Settlement Offer to Halsted Financial Services

You’re almost at the finish line! After determining what you can comfortably pay via lump sum or monthly payments, it’s time to write up a settlement offer.

📌 Upsolve Tip: Use Upsolve’s Debt Settlement Letter Template to get started. Ask Halsted Financial Services to respond to your letter in writing as well. This ensures you always have a written record of the agreement. Usually, debt collectors send settlement agreements in the mail, so make sure you scan, take a picture of, or retain the original letter for your records.

Don't Just Negotiate the Amount… Negotiate Everything!

In addition to negotiating the settlement amount, you can negotiate how debt collectors report settled accounts. Accounts are usually noted on your credit report as paid in full, partial payment, or settled. In your settlement letter, ask them to report your account as paid in full to the major credit bureaus. This can help improve your credit score.

Can You Still Negotiate a Settlement if There's a Debt Lawsuit Against You?

Yes, you can still pursue a debt settlement even if you've been sued by Halsted Financial Services. However, you still need to respond to the lawsuit and comply with any court requirements, like appearing online or in person.

It’s crucial to pay attention to and respond to the lawsuit until you reach a settlement and it’s submitted to the court or until the court case is dismissed or closed.

Tips for a Successful Debt Settlement

Settling your debt is easier than you might think. Here are Upsolve’s top tips for a successful settlement.

You can read Upsolve’s article 5 Solid Steps for Negotiating With Debt Collectors to learn even more.

Can Halsted Financial Services Sue Me?

While getting sued by a debt collector is a possibility, Halsted is unlikely to sue you because they don’t own your debt.

What influences a debt collector’s decision to sue? They’ll usually consider:

The size of the debt

How much it’ll cost to sue you

If they can collect interest, court costs, and attorney fees

How easy it would be to get a court order to garnish your wages

If you have any other unpaid debts

How old the debt is and what its statute of limitations is

Applicable state laws relating to creditor rights and contracts

If Halsted decides to sue you, you’ll probably learn of the lawsuit when you’re served a copy of the complaint and summons by mail or in person. Even if you disagree with the lawsuit, you still need to respond to the complaint or you risk losing automatically.

You don’t have to hire an attorney to respond to the complaint.

How To Beat Halsted Financial Services in a Debt Lawsuit

If you've received notice of a lawsuit (a summons and complaint), it’s important to respond quickly. If you don’t, you could automatically lose your case. If the debt collector wins, they can get a court order that allows them to garnish your wages.

Responding is simpler than you might think. Many courts provide forms and instructions. The first thing to do is file an answer form or seek legal assistance. Responding protects your rights and allows you to present your defense.

If you're worried about responding on your own, but you can't afford a lawyer, you can draft an answer letter for a small fee using our partner Solo. They've helped hundreds of thousands of people respond to debt lawsuits, and they have a 100% money-back guarantee.

Solo is an affiliate partner, which means Upsolve may earn a small commission if you choose to use their paid service. This helps keep our services free.

Step 1: Read the Summons and Complaint Carefully

A summons is a court document that notifies you of a lawsuit.

It usually contains the following information:

Court name and address

Parties involved (the plaintiff is the person suing; the defendant is the person being sued)

Case number

Instructions to the defendant

Legal consequences if you fail to respond to the lawsuit

The amount of days you have to file your answer

The information in a summons can vary, especially how many days you have to respond, so be sure to read your summons carefully. A complaint is another court document that outlines the plaintiff’s claims against you. You’ll use the information in the complaint when you fill out your answer form.

Step 2: Fill Out an Answer Form (and Any Other Required Forms)

Don’t ignore a summons and complaint from Halsted Financial Services. Many courts offer blank answer forms, making it easier for you to file an answer. Google the court name on the summons followed by "answer form" or "court forms" to find an answer form.

Carefully read and follow the instructions provided on the documents. If you can’t find an answer form or don’t know how to proceed, contact the court clerk. While they can’t give you legal advice, they can let you know what paperwork you need and where you can find the documents to submit your answer.

The answer form is your chance to raise affirmative defenses. These are legal statements that could defeat or reduce the plaintiff's claims to the court.

For more information on affirmative defenses and how to defend yourself against a lawsuit, read Upsolve’s article 3 Steps To Take if a Debt Collector Sues You.

If you deny any allegation or make affirmative defenses, then file your supporting documents, such as payment records or communications, with your answer.

Some courts may require additional forms, like a certificate of service. Check the court website or consult the clerk of court to see if you need to include other forms with your answer.

As mentioned, if you don’t feel comfortable doing this on your own, you can work with SoloSuit for a small fee.

Step 3: File the Answer Form With the Court and Serve on the Plaintiff

The process of filing your answer form also varies by court. Typically, you can file in person at the courthouse or send the form via mail. You may also be able to email or e-file the form.

Sometimes, there will be a fee to file your answer. To see if there’s a filing fee or request a waiver, speak with the court clerk.

You usually need to deliver a copy of your answer form to the person suing you. This is called service. You can serve the form via mail using the address listed on the summons. Be sure to comply with any specific delivery instructions provided by the court or outlined in the summons.

How To Recover From Debt and Collections

Having a debt sent to collections is usually a symptom of a greater financial issue — often one that comes after a medical issue, job loss, divorce, or other emergency.

The good news is that no matter what your finances look like right now, you can bounce back and move forward.

If you’re struggling with multiple credit card debts and can’t figure out how to stay afloat, consider speaking with a nonprofit credit counselor. They can help you understand your options and may suggest a debt management plan to bring debt payments under control and save you money on interest and fees. Or they may discuss Chapter 7 bankruptcy for a total fresh start.

You can often negotiate or get help with large medical bills. And you can always try renegotiating or refinancing big loans like mortgages or car loans.